The Influence of the Inflation on the Efficiency of the US Greenback

Inflation is likely one of the key macroeconomic forces shaping monetary markets, influencing asset costs throughout the board. In our earlier evaluation, we examined how gold and Treasury costs react to adjustments within the inflation fee, uncovering patterns that urged inflation dynamics additionally influence the US Greenback. On this follow-up, we shift our focus solely to the greenback, analyzing the way it responds to each accelerating and decelerating inflation. Because the world’s reserve foreign money, the greenback’s actions have far-reaching implications, affecting international commerce, financial coverage, and asset allocation. Our objective is to find out whether or not inflation serves as a transparent driver of greenback efficiency and, in that case, in what methods.

Background

As a macroeconomic variable, inflation considerably influences numerous asset lessons, together with equities, fixed-income securities, and commodities. The connection between inflation and asset efficiency is complicated and multifaceted. As an example, empirical research reminiscent of these by Bernanke et al. (1996) spotlight how inflationary shocks propagate by way of the monetary accelerator mechanism, affecting credit score provide and asset valuations. Within the fixed-income market, inflation erodes the actual returns on nominal bonds, as articulated by the Fisher equation. Our personal article uncovers, that acceleration within the inflation fee is a optimistic for gold costs, whereas however, deceleration within the inflation is advantageous to the treasury costs. Moreover, Gopinath (2015) demonstrates that extended low rates of interest can paradoxically hinder financial progress and inflation targets, emphasizing the necessity for a nuanced understanding of those dynamics.

The connection between inflation and the efficiency of the U.S. greenback can be sophisticated and many-sided. An increase in inflation can weaken the US Greenback in opposition to a basket of different currencies if it erodes buying energy and diminishes confidence within the foreign money’s stability. If inflation surges with out a proportional improve in rates of interest or if markets anticipate that the Federal Reserve will lag in its response, the actual return on dollar-denominated property declines. This may result in capital outflows as buyers search property in international locations with extra steady or increased actual yields, driving the greenback decrease. Moreover, increased home inflation can cut back the competitiveness of US exports, widening the commerce deficit and additional pressuring the foreign money.

However, a decline in inflation can strengthen the greenback if it alerts financial stability and prompts the Fed to keep up and even tighten financial coverage relative to different central banks. Decrease inflation preserves the greenback’s buying energy, making it extra enticing as a retailer of worth. If different economies proceed to expertise increased inflation whereas the US sees inflation cooling, relative financial coverage divergence can drive buyers towards the greenback, rising its worth in opposition to different currencies.

Let’s not waste extra time with the speculation and transfer to the outlines of our investigations.

Discovering 1 — Influence of Inflation Alone

As our earlier evaluation hinted, the US Greenback can be delicate to inflation (albeit with a decrease amplitude than gold or treasuries), and we will, subsequently, outline our primary easy benchmark funding technique with the next buying and selling resolution guidelines:

If inflation rises (for 2 consecutive months), take a brief place on USD and maintain it till the other sign arrives.

If inflation declines (for 2 consecutive months), take a protracted place on the USD and in addition maintain it till the other sign arrives.

In easy phrases, we’re switching between two positions (lengthy/quick USD) primarily based on the final inflation sign (deceleration/acceleration). The fairness curve graph presents the technique’s efficiency (which exhibits a sluggish appreciation of capital over time). What can we are saying concerning the outcomes? Effectively, there’s positively sturdy efficiency between the years 1990 and 2005, when inflation alone efficiently predicted actions within the US Greenback. Nonetheless, the ends in the final years are blended, so there’s room for enchancment.

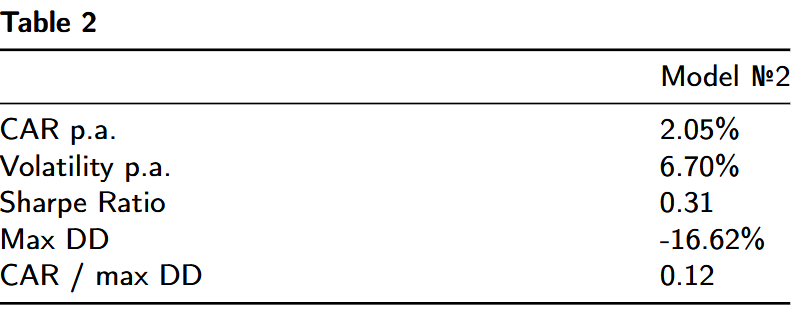

Discovering 2 — Influence of FED Charge

Naturally, the FED has a say concerning inflation and endeavors to fight it. So, we shaped our second rule:

As outlined, we’re within the “FED Up” interval after the primary fee hike, and we change if the FED cuts charges.

We’re within the “FED Down” interval after the FED cuts charges, and we change if the FED raises charges.

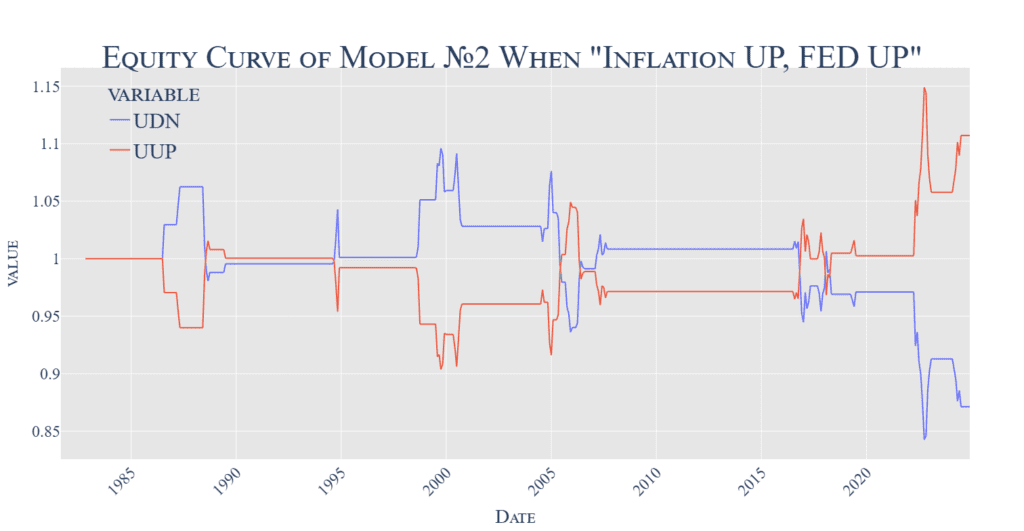

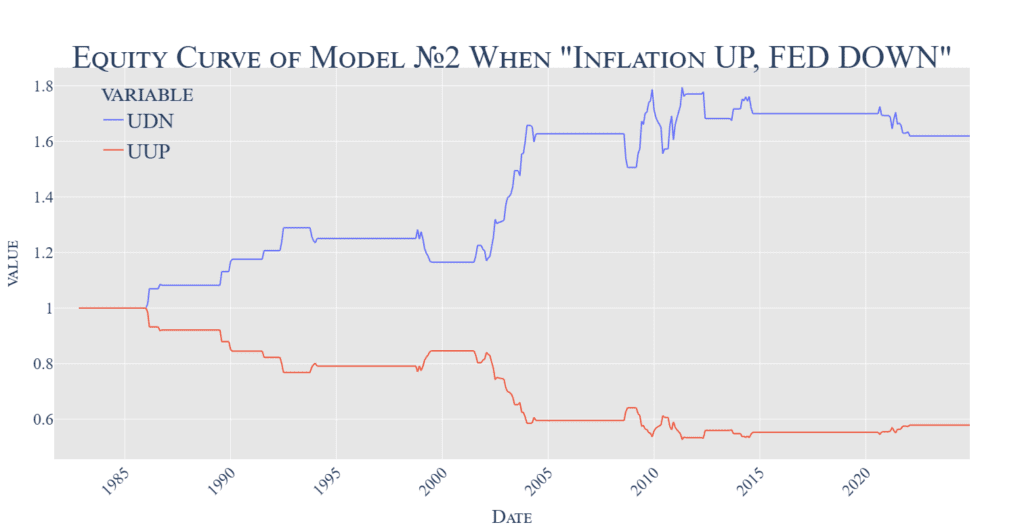

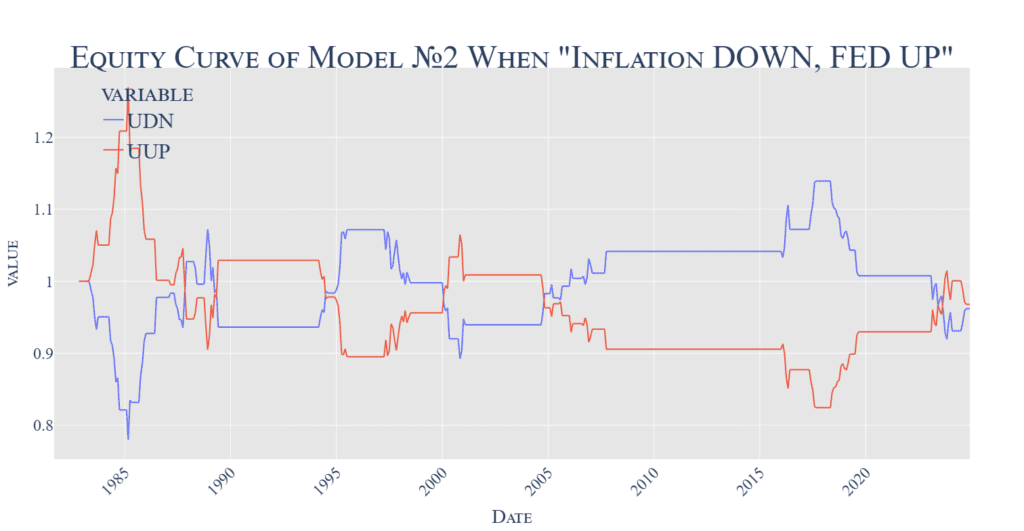

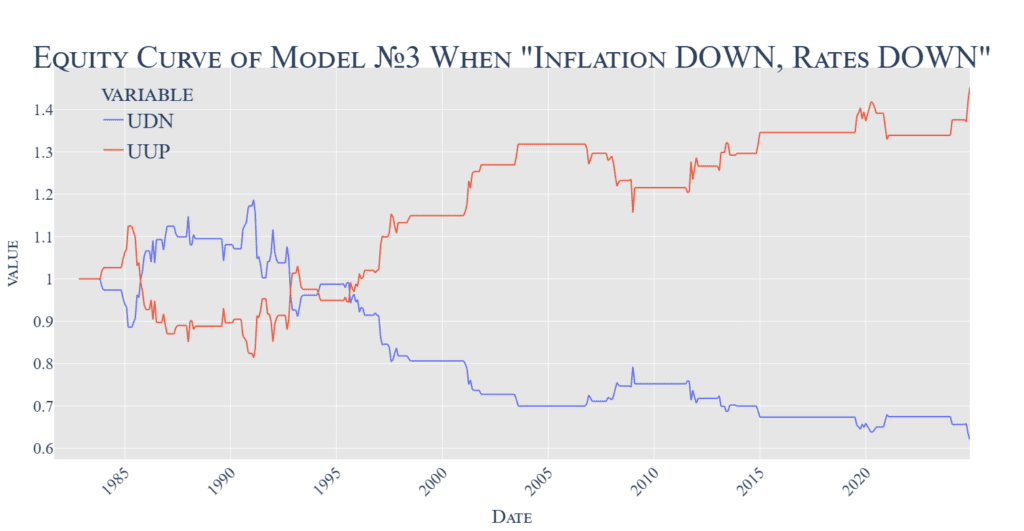

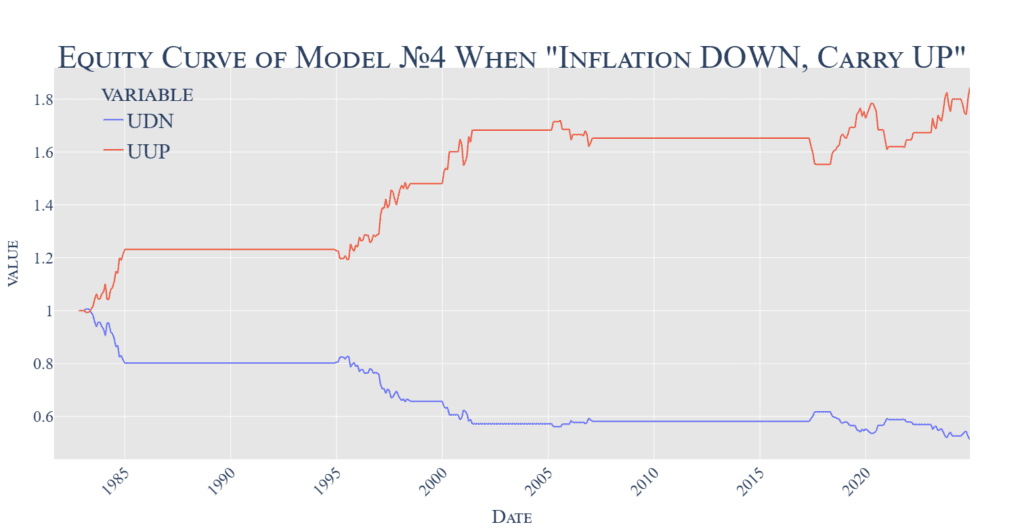

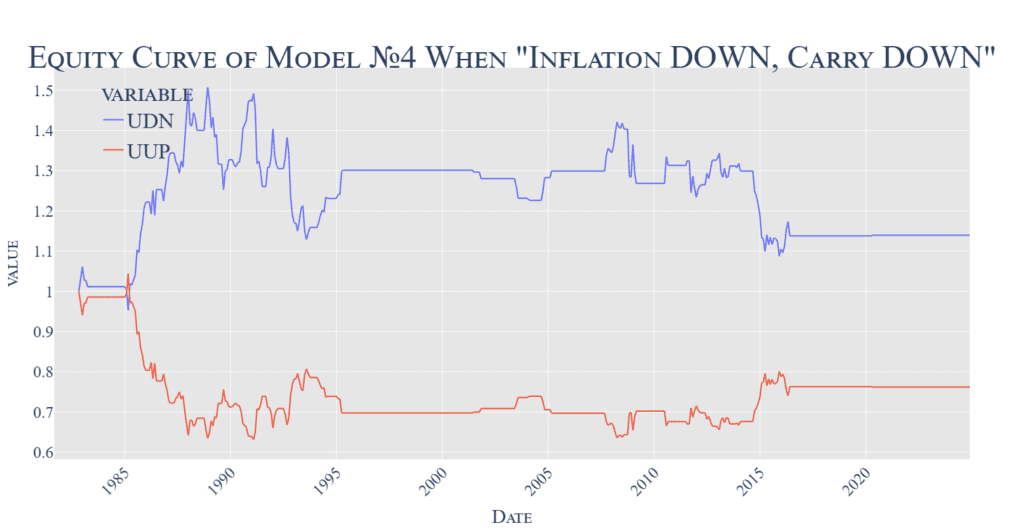

In complete, we will have 4 completely different market epochs, primarily based if we divide the entire historical past primarily based on 2 completely different predictors. The 4 graphs beneath signify situations the place inflation decelerates/accelerates and FED cuts/will increase. We use 2 completely different ETFs as an funding car, one for the quick USD place (UDN – Invesco DB US Greenback Index Bearish Fund) and one for the lengthy USD place (UUP – Invesco DB US Greenback Index Bullish Fund).

Now, what could possibly be the takeaway?

It’s advantageous to go lengthy USD if inflation decelerates and the FED concurrently cuts charges.

Secondly, it’s a good suggestion to quick USD if inflation rises and the FED cuts charges (which could be an misguided central financial institution coverage).

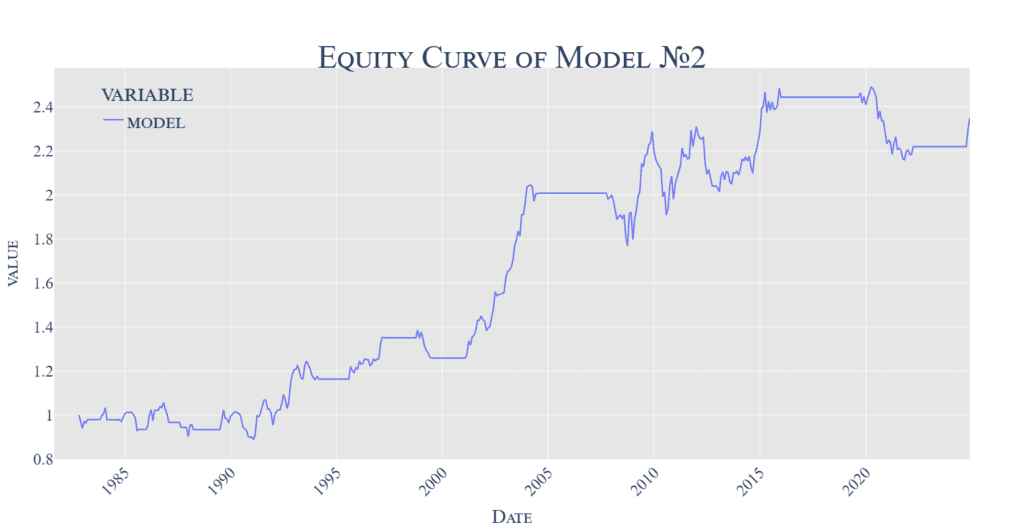

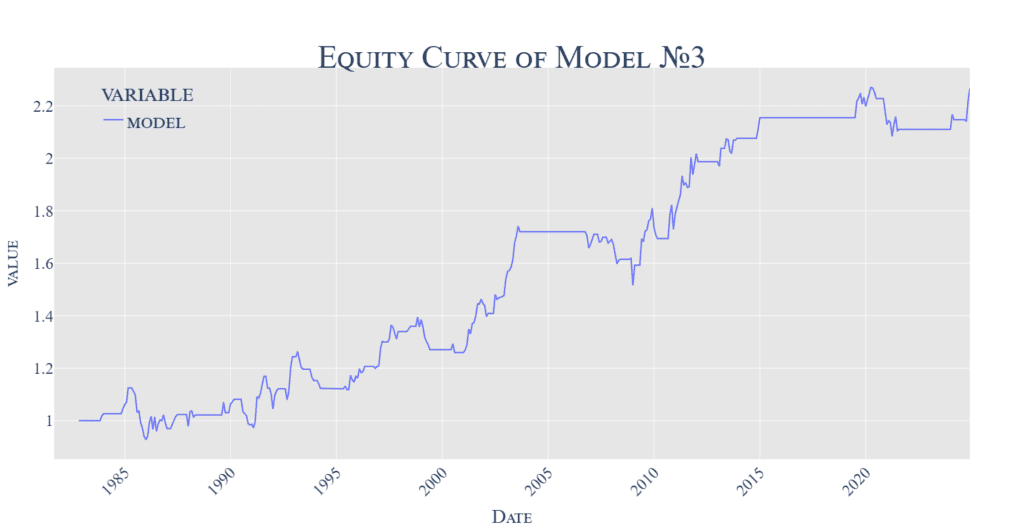

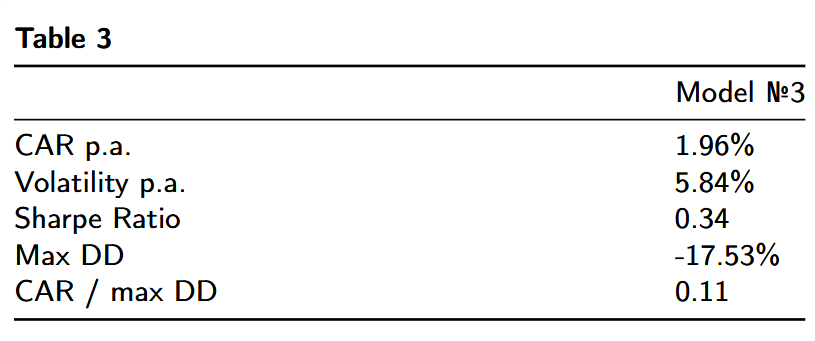

We are able to combine these 2 guidelines right into a blended technique with the next outcomes:

Integration of the details about the FED coverage and inflation sign into one technique clearly outperforms the essential benchmark technique, which makes use of simply the inflation sign alone. Nonetheless, the FED coverage shouldn’t be the one sign we will attempt.

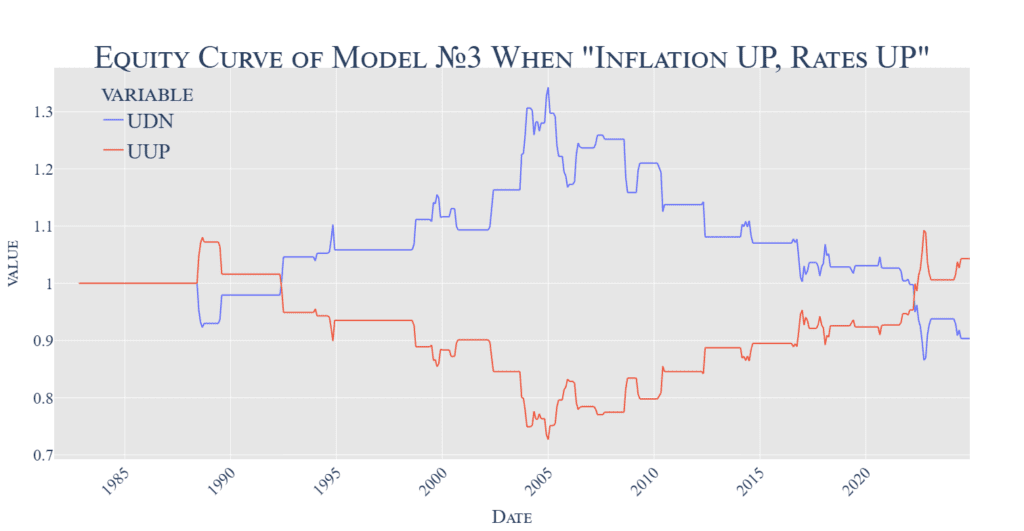

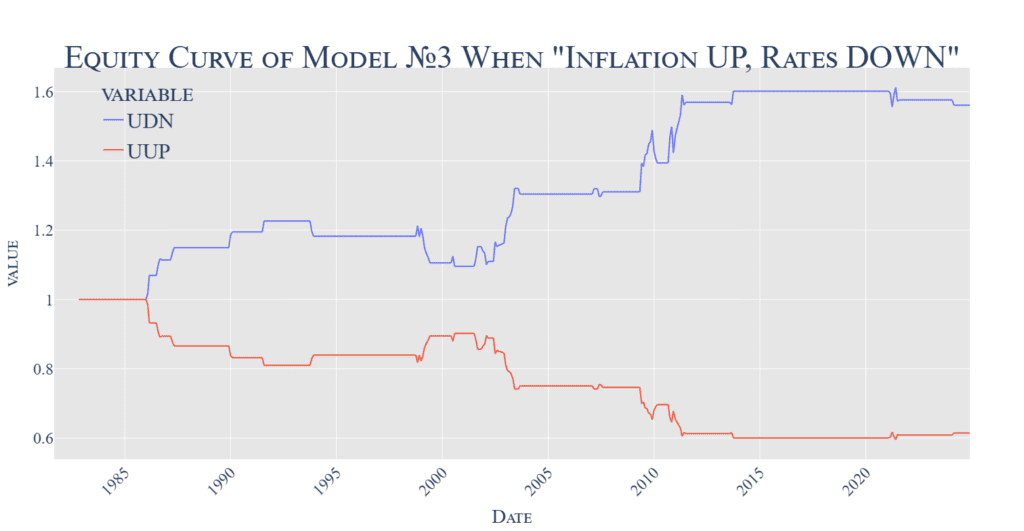

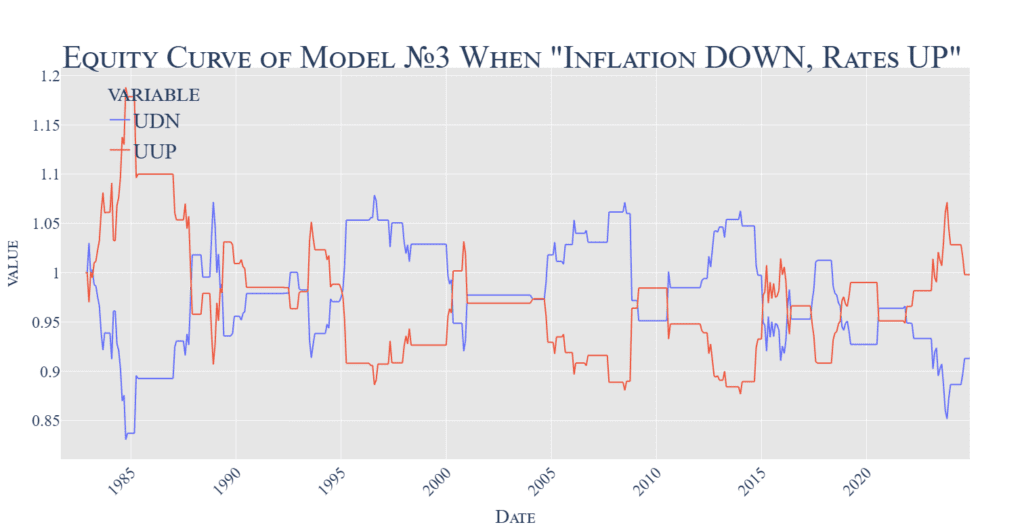

Discovering 3 — Affect of the 3-Month Charge

As a substitute of utilizing the FED fee to sign an rising or reducing fee interval, we will use the 3-month treasury charges, and base our sign on the identical logic as we have now for the inflation. Subsequently:

If 3-month charges rise (for 2 consecutive months), we’re in a “Charges UP” interval.

Alternatively, if 3-month charges lower (for 2 consecutive months), we’re in a “Charges DOWN” interval.

Now, let’s observe the outcomes of the lengthy USD/quick USD substrategies from 4 scenario-based graphs:

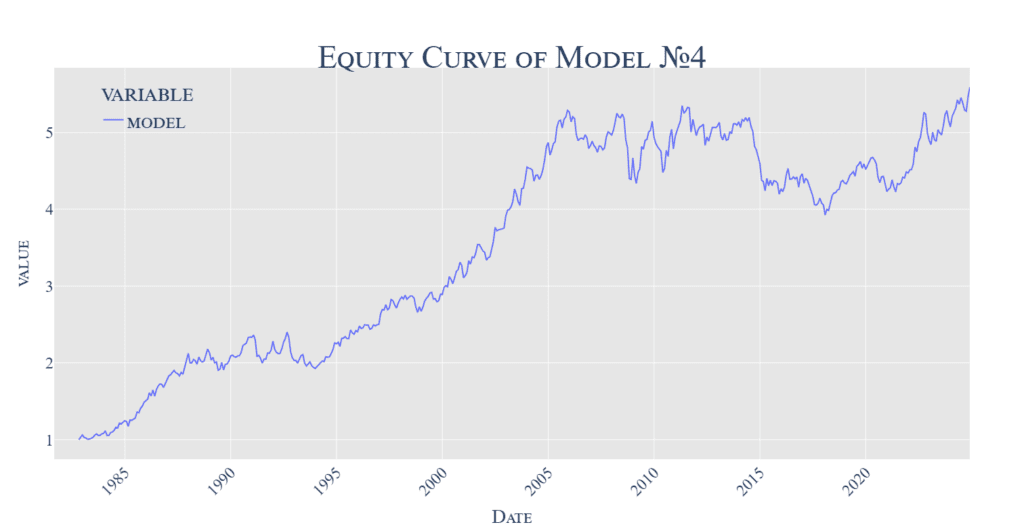

So, the mixed sub-strategies utilizing the 3-month charges and inflation are very comparable than sub-strategies utilizing the mixture of the FED fee and inflation. It’s advantageous to go lengthy USD if inflation decelerates and the 3M charges go down. Concurrently, it’s a good suggestion to quick USD if inflation rises and the 3M charges goe down (which could once more sign an misguided central financial institution coverage).

The resultant buying and selling technique has comparable return-to-risk ratios than Mannequin no.2, albeit with barely completely different durations when it performs nicely. Theoretically, the alerts from Mannequin no.2 and Mannequin no.3 can most likely be mixed for a extra strong technique. Nonetheless, we don’t plan to discover this chance in the mean time, as there’s another prediction sign that goes nicely together with the inflation sign.

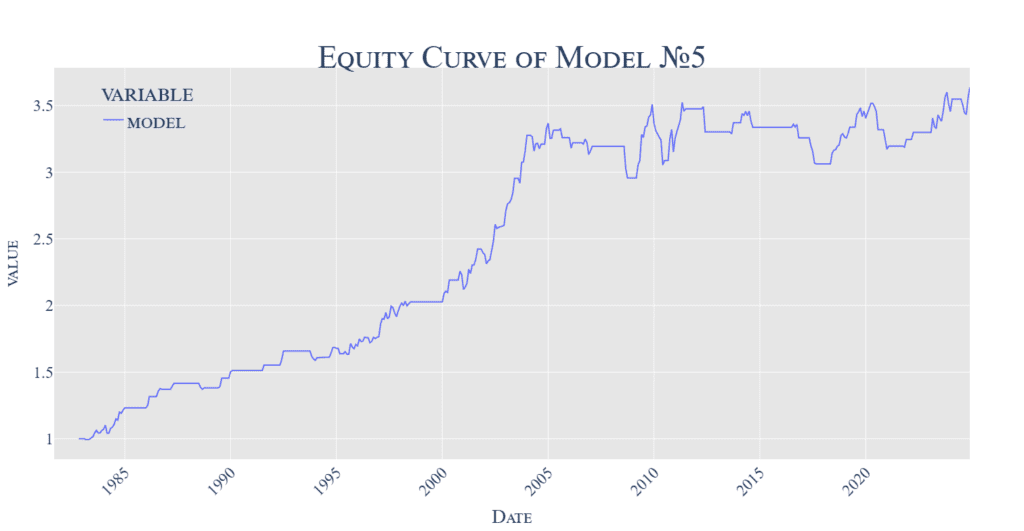

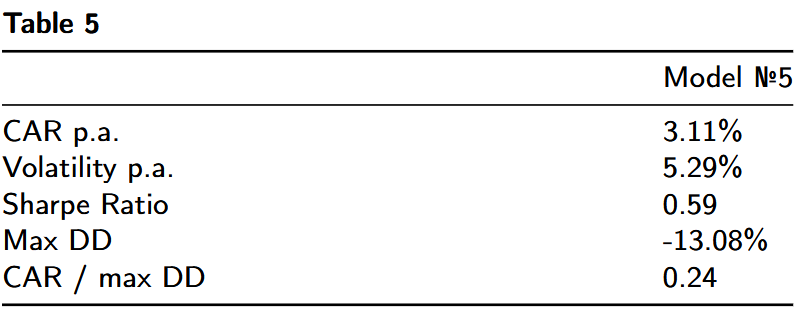

Discovering 4 — Influence of Curiosity Charge Differentials

The US Greenback foreign money shouldn’t be alone in our world, and absolutely the measure of the US economic system or absolutely the measure of the extent of rates of interest can be not an important driver for the efficiency. Relative standing and relative measures are essential, too, and some of the essential measures is the rate of interest differential between the risk-free fee within the US Greenback and different currencies – the Carry yield. We are able to use distinction between the US 3-month fee and the common 3-month fee of six different main international currencies (EUR, CAD, CHF, GBP, AUD and JPY) as our predictor and outline a easy US Greenback Carry Commerce as:

Lengthy USD if it has a better fee than the common of different international locations, and

quick within the reverse case.

Naturally, inflation additionally performs a task. So, now we will attempt to pair the rate of interest differential sign with the inflation sign in our mannequin, too:

The earlier figures present higher efficiency after we go lengthy USD if it has increased charges than the remainder of the world (and it doesn’t matter, what’s the inflation doing). Conversely, quick USD when inflation accelerates, and the US Greenback has decrease charges than the remainder of the world.

Combining the inflation sign with the carry sign achieves higher ratios resulting from decrease threat. Nonetheless, the ultimate technique nonetheless struggled after 2010, as many of the different currency-carry methods have been as a result of low yields within the monetary repression period between 2008 and 2018.

Our analysis findings present important insights into the complicated dynamics governing the US greenback’s conduct, inflation, and rates of interest. A few of our outcomes problem standard knowledge, notably when the Federal Reserve cuts charges throughout declining inflation. The optimistic efficiency of USD in these circumstances means that market interpretations of financial coverage actions are extra nuanced than typically assumed.

In all the instances, the inclusion of the 2nd predictor primarily based on the rates of interest sign (whether or not it’s FED fee, 3M fee, or rate of interest differential) improves the return-to-risk ratios compared to the bottom technique that makes use of simply sign from the inflation alone. However, in many of the methods, there’s a seen lower within the efficiency within the period of economic repression (2008-2018), when the motion within the US greenback was tougher to foretell. We’re eager to watch how all the methods will carry out within the subsequent few years and if the return of inflation and better rates of interest within the final years will return, in addition to the upper predictability of the US greenback change fee.

Writer: Cyril Dujava, Quant Analyst, Quantpedia

Are you in search of extra methods to examine? Join our e-newsletter or go to our Weblog or Screener.

Do you wish to be taught extra about Quantpedia Premium service? Test how Quantpedia works, our mission and Premium pricing provide.

Do you wish to be taught extra about Quantpedia Professional service? Test its description, watch movies, assessment reporting capabilities and go to our pricing provide.

Are you in search of historic knowledge or backtesting platforms? Test our checklist of Algo Buying and selling Reductions.

Or comply with us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookSeek advice from a pal