Worry, Not Danger, Explains Asset Pricing

With monetary markets more and more whipsawed by geopolitical tensions and unpredictable coverage shifts from the Trump administration—traders are as soon as once more questioning perceive threat, worry, and the true drivers of returns. A current and compelling paper dives into this debate with a provocative thesis: in “Worry, Not Danger, Explains Asset Pricing,” authors Rob Arnott and Edward McQuarrie argue that conventional fashions constructed on quantifiable threat have failed to clarify real-world returns, and that worry—messy, emotional, and deeply human—is the lacking piece.

The authors start by difficult the foundational assumptions behind conventional risk-based fashions just like the Capital Asset Pricing Mannequin (CAPM) and the Environment friendly Market Speculation. They current a historic and empirical post-mortem of the concept that taking over extra threat essentially results in larger returns. Their evaluation exhibits durations—some lasting many years—the place equities did not outperform supposedly “safer” authorities bonds, each within the U.S. and internationally. Removed from being anomalies, these episodes are seen as repeated failures of threat principle to clarify precise investor outcomes. As a substitute, Arnott and McQuarrie argue that human feelings—particularly worry of loss (FoLI) and worry of lacking out (FoMO)—provide a extra compelling clarification for investor conduct and asset worth motion over time.

They suggest a brand new paradigm, one that’s investor-centric fairly than asset-centric, constructed not on tidy math however on behavioral truths. Underneath this framework, worry is multi-dimensional and dynamic, oscillating between panic and euphoria. It explains every little thing from meme shares to market crashes, and even why traders pile into low-yield property regardless of realizing the maths doesn’t add up. This mannequin—the so-called Deranged Asset Pricing Mannequin (DAPM)—doesn’t discard conventional threat metrics, however it means that our fashions are “searching for keys beneath the lamppost” whereas the actual drivers of returns disguise within the emotional darkish alley of investor psychology.

Authors: Robert D. Arnott and Edward F. McQuarrie

Title: Worry, Not Danger, Explains Asset Pricing

Hyperlink: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5127501

Summary:

Danger principle has dominated the asset pricing literature for the reason that Sixties. We chronicle empirical failures of threat principle in its prediction of the surplus return on equities, to put the groundwork for a complementary framework, investor-focused fairly than asset-focused, and centered on worry fairly than goal measures of threat. A worry premium places worry of lacking out on a par with worry of loss. Most anomalies and components of the previous half-century would have been anticipated, given a fear-based mannequin for returns. The brand new paradigm is obtainable as a place to begin to advance funding science.

As at all times, we current a number of attention-grabbing figures and tables:

Notable quotations from the tutorial analysis paper:

“The worry paradigm doesn’t dispute that human traders are loss averse. FoLI, worry of shedding it, motivates many human funding selections. However the worry paradigm has a broader definition of loss. FoMO—lack of achieve or alternative value—could also be simply as aversive as lack of principal, particularly when a bull market fosters boundless optimism. A assured return of solely two foundation factors, when 30% returns could also be accessible, is aversive. It might probably solely be overcome by some larger aversion, as when a mortgage shark threatens. Once more, human traders are afraid of many issues. There could be no significant wealth accumulation at two foundation factors per 12 months. For the human investor, it may be simply as scary to by no means get wherever as to lose a few of what one already has.

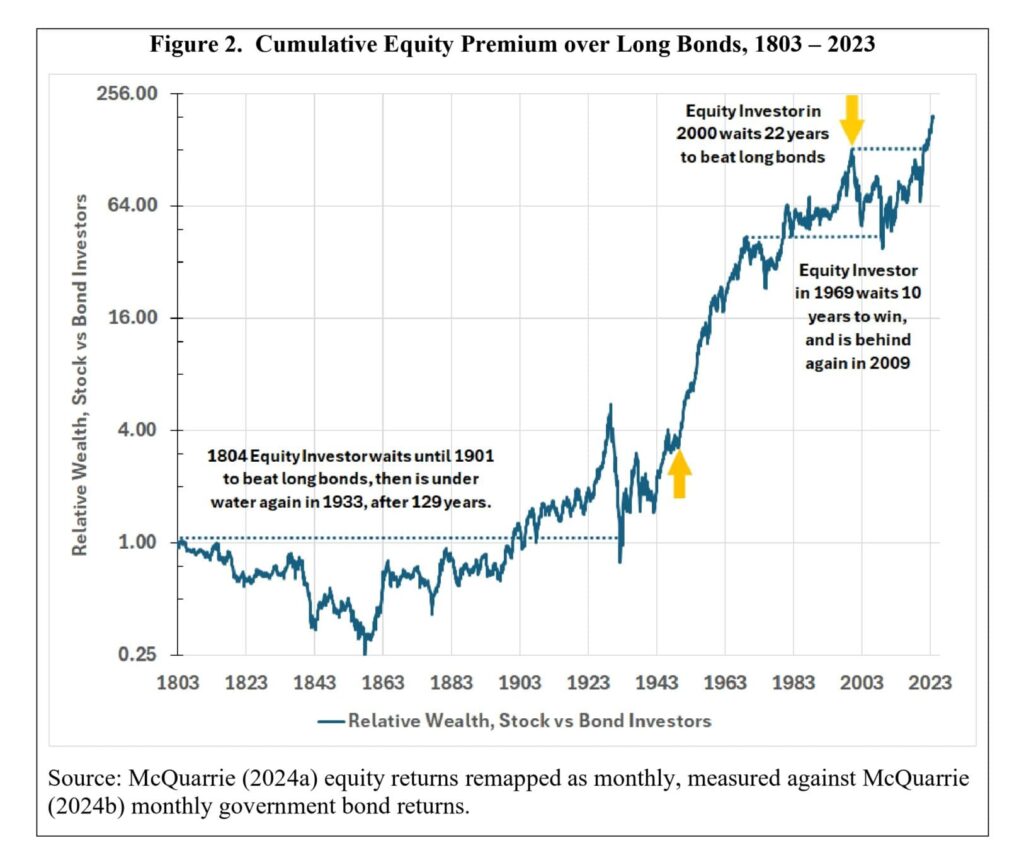

Nevertheless, these preliminary outcomes have been topic to dispute, insofar as McQuarrie’s measure of bond returns previous to 1926 had typically included company bonds in addition to authorities bonds. Given their extra idiosyncratic dangers, inclusion of company bonds undercut the specified comparability of a extra to much less dangerous asset. Extra lately he addressed that objection by setting up a brand new measure of bond returns from 1793 that makes use of authorities bonds solely, and Treasury bonds every time accessible (McQuarrie 2024b). Determine 1 plots the actual fairness premium or deficit over the rolling 10-year (120-month) spans from January 1793 to December 2023 utilizing that new authorities bond index and the McQuarrie (2024a) inventory returns. Fairness deficits are noticed time and again, in recent times in addition to within the 19 th century. Determine 2 exhibits that traders typically needed to wait till their great-grandchildren have been totally grown earlier than receiving a cumulative revenue from exhibiting a desire for equities. It bears point out that these outcomes are for the US, which has had among the many finest long-term actual inventory market returns on this planet (Jorion and Goetzmann 1999).

These outcomes will not be suitable with the speculation that threat, as measured by customary deviation, offers an index of the rewards that traders demand to obtain, i.e., that riskier property are priced to ship larger returns when held for an extended interval. Danger fails the check of precision; or extra precisely, the precision of threat is a distraction, with its exact measurement not panning out so far as prediction is worried.

Danger principle would appear to foretell that pre-SEC inventory market returns would have needed to be larger, to account for the larger threat of inventory investing earlier than that protecting laws was put in place. Rephrasing the quote from Goetzmann and Ibbotson, the nineteenth century inventory investor would have demanded a larger fairness threat premium, to replicate the a lot larger risks of inventory investing within the many years earlier than the brand new securities laws. Likewise, post-Thirties returns ought to be comparatively decrease for shares, given the substantial discount in threat as soon as the SEC was on the beat.

However historical past exhibits in any other case. Determine 5 splits the file on the finish of 1935, and charts actual returns over the prior 65 years to the start of the Cowles (1939) knowledge, and ahead 65 years to the tip of 2000. Given the tumultuous occasions surrounding the laws, Determine 5 grays out the 5 years on both facet of that hinge date, and the quantitative evaluation compares outcomes from earlier than 1931 with outcomes after 1940.28

Historic knowledge present an excessive amount of mispricing of fairness values for this derangement to have issued from rational selections made collectively by risk-averse actors. Worry positively predicts mispricing, and the extent to which mispricing is seen and customary, out on this planet of investing, offers supporting proof for the worry paradigm. Extra typically, derangement implies that markets will likely be tough to foretell utilizing any goal issue akin to threat. What traders worry at any given second is topic to fixed change. Generally there’s a flight to security. Generally there may be worry of lacking out. In that sense, DAPM is totally in keeping with these variations of the Environment friendly Market Speculation which maintain that future inventory returns are tough to foretell.”

Are you searching for extra methods to examine? Join our publication or go to our Weblog or Screener.

Do you need to study extra about Quantpedia Premium service? Verify how Quantpedia works, our mission and Premium pricing provide.

Do you need to study extra about Quantpedia Professional service? Verify its description, watch movies, evaluate reporting capabilities and go to our pricing provide.

Are you searching for historic knowledge or backtesting platforms? Verify our listing of Algo Buying and selling Reductions.

Or comply with us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookConsult with a pal