Our aim with The Every day Temporary is to simplify the largest tales within the Indian markets and provide help to perceive what they imply. We received’t simply let you know what occurred, however why and the way too. We do that present in each codecs: video and audio. This piece curates the tales that we speak about.

You’ll be able to take heed to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and movies on YouTube. You can too watch The Every day Temporary in Hindi.

In at the moment’s version of The Every day Temporary:

Hospitals ship robust outcomes

What do RBI surveys say about India’s future?

The Q3 outcomes for India’s greatest hospital gamers are out. As we speak, we’re two of the largest names in non-public healthcare — Apollo Hospitals and Fortis Healthcare. Each had nice quarters. They each noticed large jumps in earnings, rising EBITDA margins, higher occupancy charges, and extra income per occupied mattress.

If this feels like Greek and Latin to you, don’t fear. We all know we haven’t coated this sector earlier than. So, earlier than we dive into the numbers, we’re going to step again and perceive India’s hospital sector. By the top of this, you’ll understand how hospitals become profitable, what drives their profitability, and why some hospitals carry out higher than others. Let’s dive in.

The place hospitals slot in India’s healthcare sector

The healthcare enterprise falls into three broad classes: major , secondary , and tertiary care.

Main care comes on the first level of contact — like your common physician, who handles routine sicknesses. Secondary care consists of native hospitals and nursing houses, which deal with extra severe medical situations, however usually don’t carry out ultra-complex surgical procedures.

Tertiary care is the place huge hospital chains like Apollo and Fortis function. These provide superior, multi-specialty remedies like organ transplants or cardiac surgical procedures. That is the place the largest income alternatives exist. These hospitals cater to insured sufferers, company tie-ups, cash-paying people, and worldwide medical vacationers, all of which might usher in substantial chunks of cash. That is the house by which most listed gamers function.

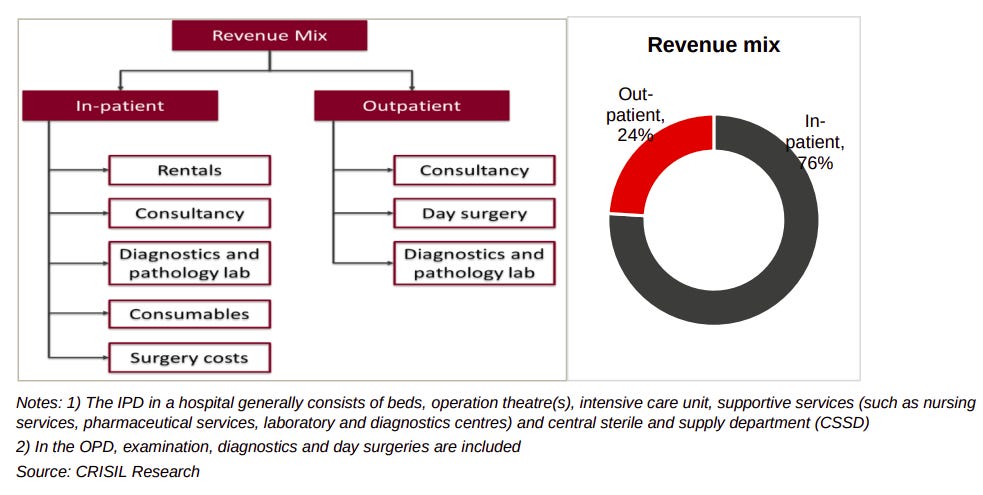

How hospitals become profitable: The OPD vs. IPD dynamic

A hospital is a posh enterprise with a number of income streams. One of the vital vital metrics to contemplate, nevertheless, are their Outpatient Division (OPD) and Inpatient Division (IPD) companies.

OPD refers to walk-in consultations, diagnostic checks, and minor remedies — the place the affected person doesn’t get admitted. IPD sufferers, alternatively, are admitted for surgical procedures, ICU stays, or long-term remedies. They incur mattress expenses, surgical charges, ICU prices, medical consumables, and pharmacy gross sales, all of that are high-margin income streams. Naturally, the latter generates essentially the most income. Whereas OPD accounts for 75-80% of hospital visits, IPD sufferers contribute 70-80% of hospital income.

Supply: CRISIL

Key Metrics That Traders Look At

Due to how essential in-patients are to a hospital’s income, essentially the most essential metrics, if you’re a hospital, revolve round admitted sufferers. These immediately decide how nicely a hospital is monetizing its infrastructure. Accordingly, past mere revenues, there are particular numbers that individuals typically have a look at:

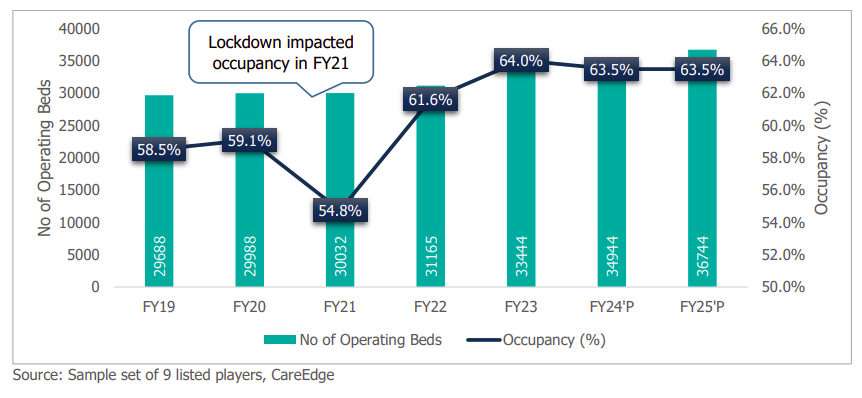

The Mattress Occupancy Price signifies how nicely a hospital is utilizing its obtainable beds. Most hospitals in India function at 60-75% occupancy.

The ARPOB (Common Income Per Occupied Mattress) displays the hospital’s pricing energy. Premium hospitals (like Apollo and Max Healthcare) command ₹40,000-₹50,000 a day, whereas value-focused hospitals (like Narayana Well being) have decrease ARPOBs however compensate with greater affected person volumes.

The ALOS , or Common Size of Keep , seems to be at how lengthy a affected person stays within the hospital. This usually falls between 3-5 days. For profitability, hospitals try to steadiness quick affected person turnover with high-value, complicated procedures.

Supply: CareEdge Scores

Past this, individuals typically take note of a hospital’s EBITDA margins to know its working profitability. Hospitals normally have large quantities of actual property and numerous very extremely expert employees — all of which make for terribly excessive mounted prices. They subsequently want robust margins to be sustainable.

Understanding payor combine

Past what number of sufferers it treats, a hospital’s income will depend on who’s paying for these remedies. Most of their income both comes from self-pay (money) sufferers or insurance coverage firms.

Money sufferers pay instantly and out-of-pocket, permitting hospitals to cost full market charges. This consists of medical vacationers, who come for high-end procedures like transplants, robotic surgical procedures, and sophisticated cardiac remedies. However, insurance coverage firms tie hospitals all the way down to negotiated charges, reducing margins barely. Additionally they stretch the timelines at which hospitals obtain cash. On the similar time, they create regular affected person volumes. Due to this fact, if you’re a hospital’s payor combine, extra out-of-pocket clients suggest higher margins, whereas the next share of insured clients factors to higher stability.

The remaining income comes from authorities schemes like Ayushman Bharat and company tie-ups.

Now that now we have a adequate understanding of how the sector works, let’s break down how Apollo and Fortis carried out in Q3. These are the highest gamers in Indian healthcare and can provide you a superb sense of what’s occurring. You need to know one factor, nevertheless: they’re not consultant of total Indian healthcare. Such hospitals cater to an elite clientele in city India, and the traits you see right here is likely to be more durable to generalize past this group.

Apollo Hospitals

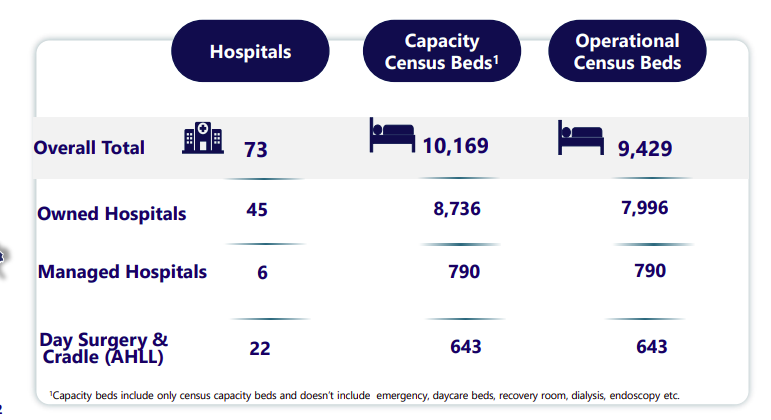

Apollo Hospitals is India’s largest non-public healthcare supplier. Over this quarter, it expanded its dominance with 73 hospitals, with over 10,000 operational beds. Past hospitals, nevertheless, it has a number of strains of income — from pharmacies to diagnostics to telehealth. This ensures that there are a number of touchpoints from which cash flows in.

Supply: Firm’s Investor Presentation

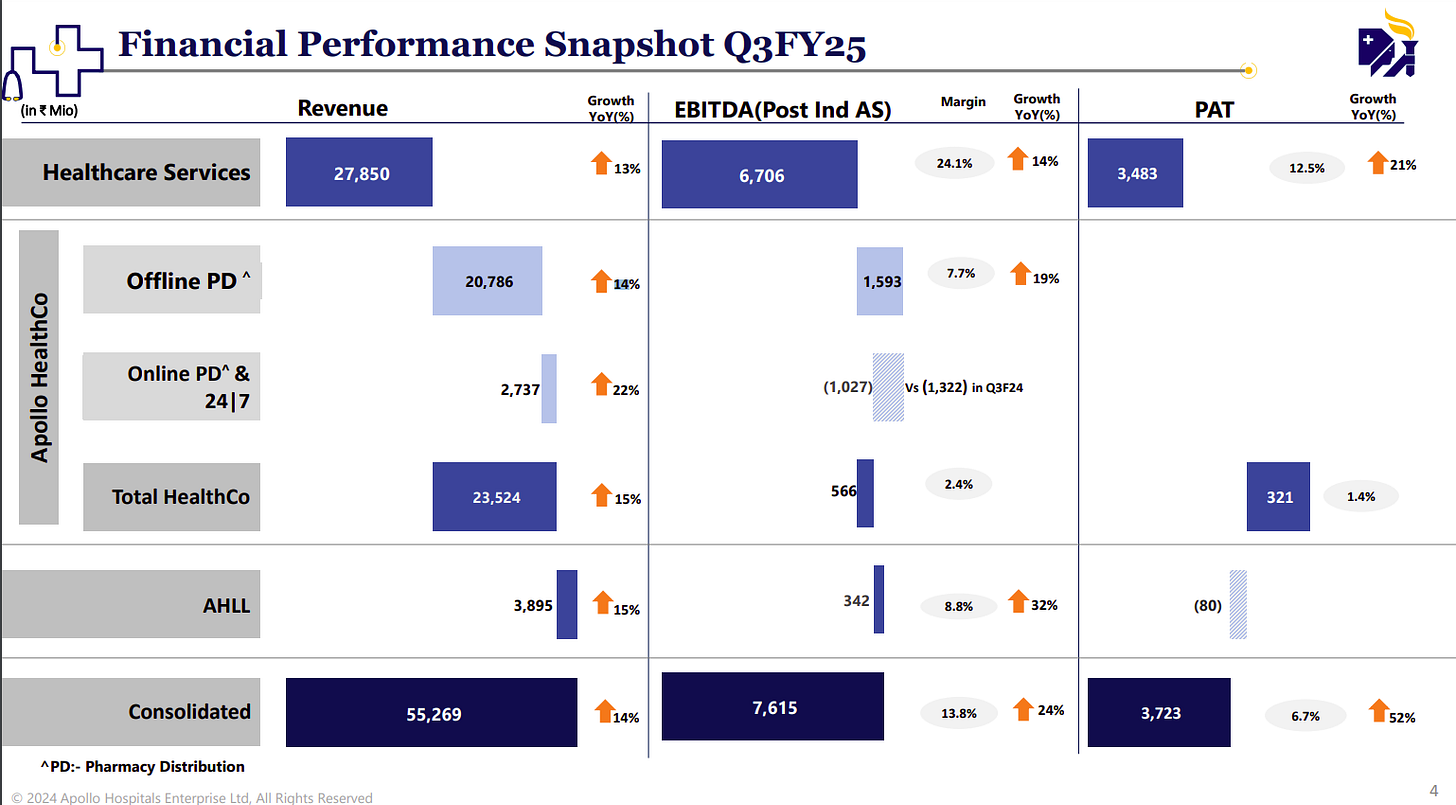

Apollo delivered a powerful Q3 FY25. Its income stood at round ₹5,527 crore, rising 14% YoY. This progress was broad-based — spanning hospitals, pharmacies, and digital well being. However past mere progress, Apollo is scaling up, increasing profitably, and making strategic shifts that enhance its long-term place.

Supply: Firm’s Investor Presentation

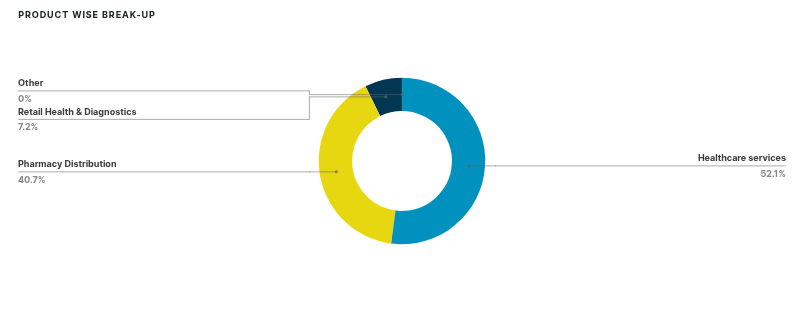

Wholesome income progress

Apollo’s hospital enterprise, which contributes 52% of its income, grew 13% YoY to ₹2,785 crore.

Supply: Tijori Finance

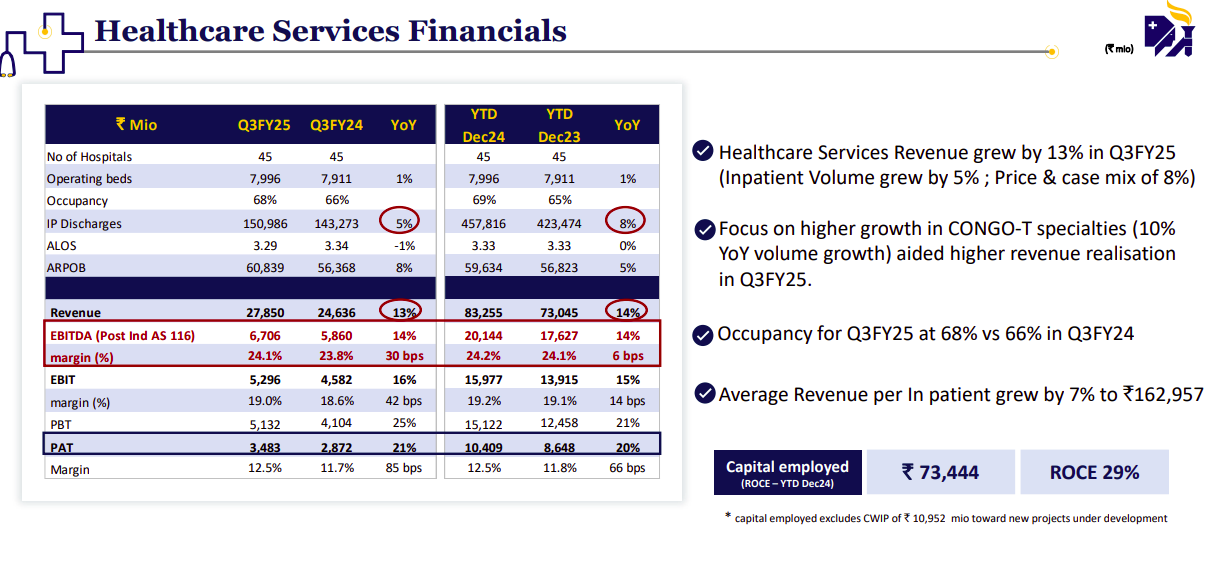

Greater and extra worthwhile affected person admissions drove this improve. The corporate noticed an 8% YoY improve in ARPOB to ₹60,839 per day, and improved mattress occupancy, at 68%.

Supply: Firm’s Investor Presentation

On the similar time, its pharmacy and digital well being section grew at 15% YoY, to ₹2,352 crore. The corporate additionally quickly scaled up its ‘Apollo 24|7’ on-line platform. This was, in truth, the primary quarter that Apollo 24|7 turned worthwhile, contributing ₹32 crore in PAT — in comparison with a ₹27 crore loss final 12 months.

That is attention-grabbing — final 12 months, Apollo offered a significant chunk of Apollo 24|7 to the PE agency Introduction Worldwide, for ₹2,475 crore. This transfer to profitability is an efficient signal for Introduction.

Higher margins, greater earnings

Past revenues, the corporate additionally improved its margins.

Apollo reported higher operational effectivity and a extra streamlined income combine this quarter. Because of this, its EBITDA margin expanded to 13.8%, from 12.7% final 12 months.

Supply: Firm’s Investor Presentation

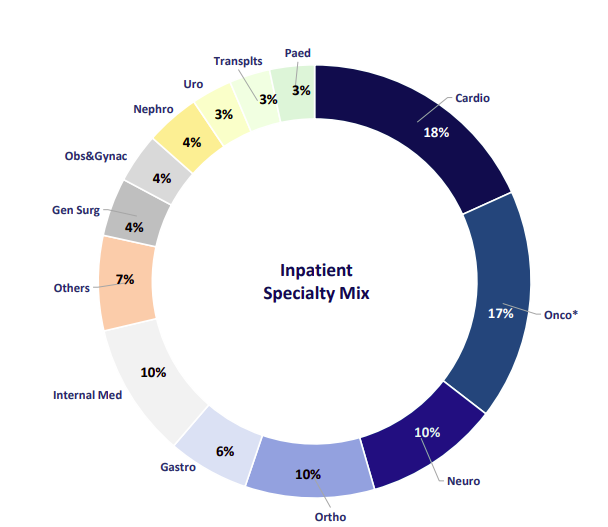

The hospital section — essentially the most worthwhile a part of the enterprise — maintained a gentle EBITDA margin of 24.1%, which is just barely greater than final 12 months. Particularly, the corporate improved its per-bed revenues — pushed by its concentrate on high-margin specialties comparable to oncology, neurology, and transplants, in addition to a rising share of worldwide sufferers, who pay premium costs.

Supply: Firm’s Investor Presentation

The turnaround of Apollo 24|7, in the meantime, sparked an extra enchancment in its margins. The quarter noticed the corporate minimize its losses on this enterprise line and switch a revenue as a substitute.

With higher margins and extra income, Apollo’s internet revenue this quarter surged by a large 52% YoY — to ₹372 crore, from ₹245 crore final 12 months.

Growth Plans and Non-public Fairness Involvement

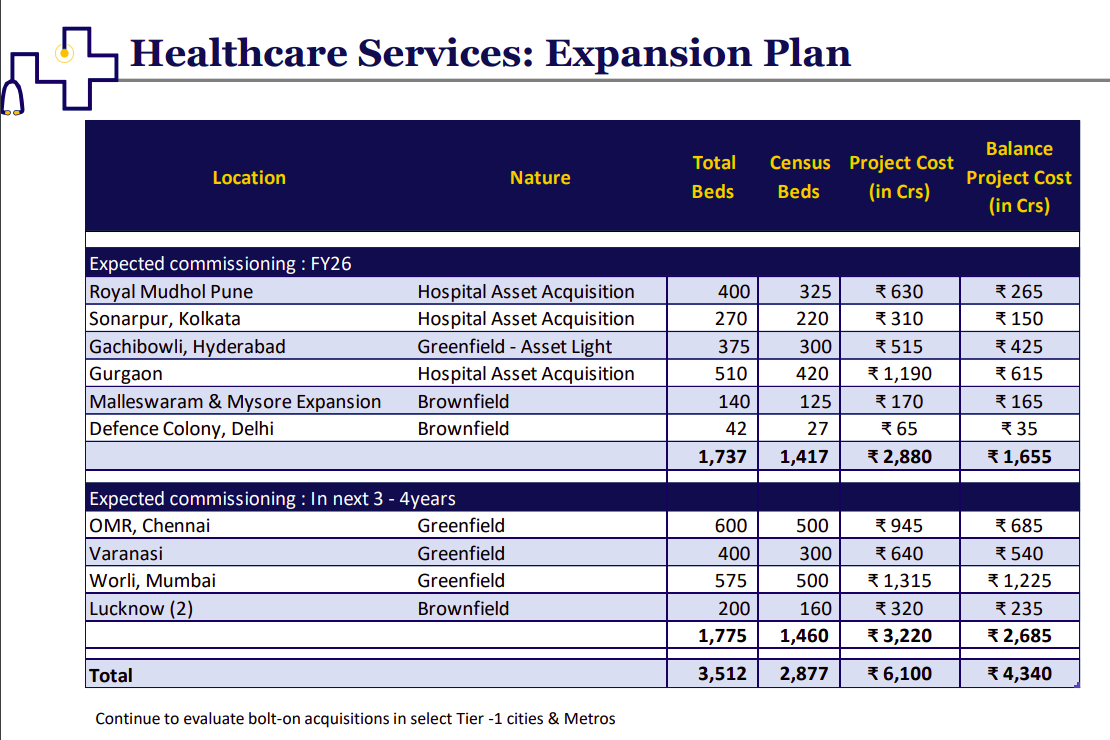

Past mere profitability figures, nevertheless, Apollo’s aggressive enlargement plans are value paying attention to.

The corporate is investing ₹6,100 crore so as to add 3,500+ beds throughout tier-1 cities like Mumbai, Chennai, Gurgaon, Hyderabad, Lucknow, and Kolkata. Quite a lot of this capital presumably got here from Introduction Worldwide — which paid the corporate ₹2,475 crore for a stake in Apollo 24|7.

The corporate’s concentrate on high-value metro places is attention-grabbing. In contrast to smaller hospital chains that broaden into Tier-2 cities for quantity, Apollo is doubling down on city facilities — the place it could cost premium charges for specialised care.

Supply: Firm’s Investor Presentation

Fortis Healthcare

Fortis Healthcare is one other of India’s main non-public healthcare suppliers. It operates 27 hospitals with roughly 4,700 operational beds throughout the nation. It was in deep monetary misery for a few years however has now mounted a powerful restoration — after receiving the backing of Malaysia’s well being big, IHH.

Whereas Apollo has diversified into digital well being and pharmacy retail, Fortis stays primarily targeted on hospitals and diagnostics. 62% of its revenues come from high-margin specialties like oncology, neurology or cardiology. In the meantime, it has doubled down on its diagnostics enterprise, Agilus Diagnostics, rising its stake from 57.68% to 89.20%.

Supply: Firm’s Investor Presentation

Income progress

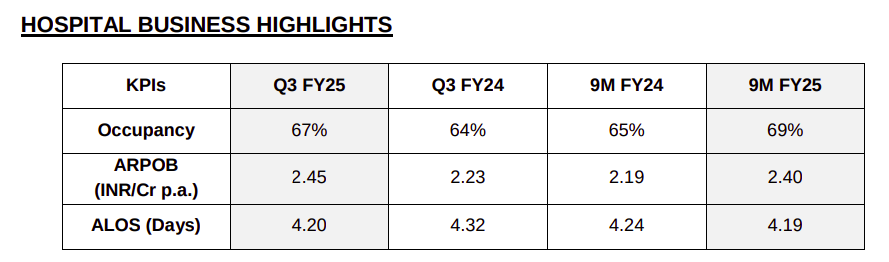

In Q3 FY25, Fortis delivered ₹1,928 crore in complete income, rising 14.8% YoY.

Its hospital enterprise, which accounts for round 84% of its complete income, grew 16.8% YoY to the touch ₹1,623 crore in income. This got here on the again of extra in-patient admissions, together with greater pricing per affected person. Its per-bed revenues rose — with ARPOB rising by 9.9%, to ₹2.45 crore each year. This reveals the corporate’s robust pricing energy and its shift in direction of extra high-value remedies. Mattress occupancy additionally improved to 67%, up from 64% final 12 months. The Common Size of Keep (ALOS) improved barely to 4.20 days.

Supply: Firm’s Investor Presentation

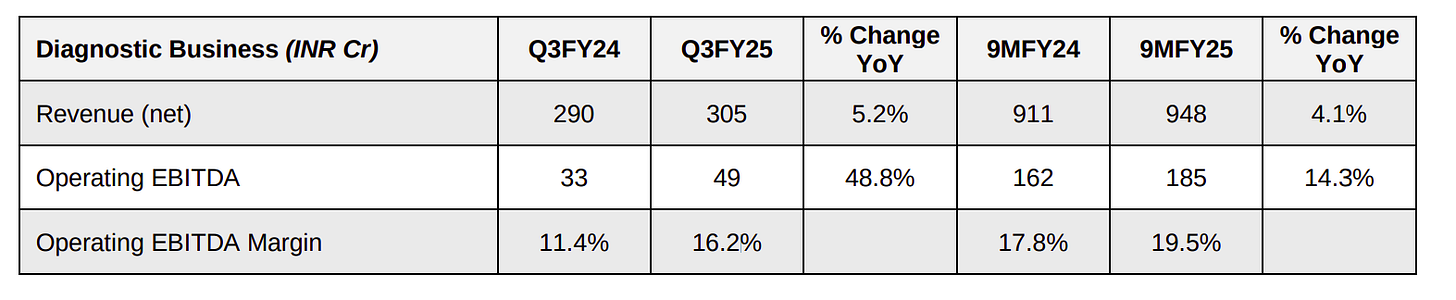

Past hospitals, Fortis’ diagnostics enterprise (Agilus Diagnostics) reported ₹305 crore in income, rising 5.2% YoY. The corporate has been busy increasing its diagnostic community, with buyer touchpoints in additional than 4,126 places.

Higher margins, greater earnings

Fortis delivered ₹375 crore in EBITDA, a 32% YoY improve, with margins bettering from 16.9% final 12 months to 19.4%.

Supply: Firm’s Investor Presentation

The hospital section, its major income contributor, noticed EBITDA margins rise to twenty.0% from 18.0% — displaying improved price efficiencies and a greater income combine. These greater margins got here from higher per-bed income, greater occupancy, and higher operational efficiencies throughout hospitals.

Its diagnostics enterprise improved its EBITDA margin as nicely — to 16.2% from 11.4% final 12 months — displaying price optimizations and extra demand for preventive checks.

Supply: Firm’s Investor Presentation

With greater revenues and higher margins, Fortis noticed its earnings soar. It posted ₹254 crore in internet revenue (PAT), up 89.5% YoY from ₹134 crore in Q3 FY24.

Streamlining the enterprise

Fortis is at the moment actively increasing its hospital community. Like Apollo, it’s targetting metropolitan areas — with most of its enlargement targeted on the Delhi-adjacent cities of Faridabad, Manesar, Gurgaon, and Noida:

Supply: Firm’s Investor Presentation

It isn’t simply rising, nevertheless. Fortis has additionally divested underperforming belongings in Bangalore and Chennai. Evidently, it isn’t merely increasing—it’s shifting its focus to high-growth areas.

The Reserve Financial institution of India (RBI) conducts a collection of ‘forward-looking surveys’ to know how individuals really feel concerning the economic system’s future. Because the title suggests, these surveys are forward-looking, As an alternative of recording exhausting information, they attempt to seize individuals’s opinions and expectations throughout totally different areas — from confidence about their employment standing to spending habits, to future mortgage demand.

A few days in the past, we coated one in all these surveys — the ‘Inflation Expectations Survey of Households (IESH).’ As we speak, we’ll have a look at all the remainder.

Why expectations matter

However earlier than we get into these surveys, it’s good to know why they’re vital.

It’s simple to ignore surveys on future expectations. In spite of everything, they’re subjective — i.e. they merely file individuals’s opinions and never goal actuality. This makes them unstable, imprecise, and infrequently deceptive. Sooner or later, individuals’s temper could also be upbeat; the subsequent, a single unhealthy headline may ship confidence crashing. Folks argue that sentiments aren’t at all times rational — they’re formed by fears, hopes, and the most recent buzz. They’re, subsequently, unconnected to the precise state of the economic system.

That’s a good level, nevertheless it additionally misses one thing essential. Whereas economists have spent many years obsessing over numbers, they’ve underplayed the ability of narratives. However narratives are vital.

Give it some thought — when an economic system slows down, do individuals run complicated financial fashions of their heads earlier than deciding to chop spending? In fact not. They react to the tales they hear — rumors of layoffs, a viral article predicting a recession, or market pundits who swear the inventory market is doomed.

Robert Shiller, the Nobel Prize-winning economist, constructed a concept round this concept in his paper Narrative Economics . He argued that tales — particularly people who faucet into feelings and unfold like wildfire — don’t simply describe financial cycles, however drive them. When narratives catch on, they affect how individuals spend, make investments, and even how governments react. In doing so, they form the economic system itself.

Shiller – Supply: Nobel Prize.org

In fact, merchants know precisely what this implies. For example, you’ve most likely seen a single bearish assertion set off panic market-wide promoting, wiping out billions in worth — not due to any elementary collapse, however as a result of sufficient individuals feared one was coming. That worry spreads, merchants react, and abruptly, the “narrative” of a collapse turns into actuality.

Supply: Weitz Funding

Such narratives are precisely what the RBI’s surveys are attempting to measure. Whereas these numbers are solely vaguely indicative of the target state of the economic system, they seize the dominant financial tales individuals are telling themselves. If Shiller is true, these narratives form the economic system as a lot as any exhausting information.

What are the surveys saying?

Now earlier than we clarify what these surveys reveal concerning the Indian economic system at the moment, allow us to make clear one factor.

In these surveys, RBI assigns a quantity to seize public sentiment on a selected side of the economic system. This quantity can vary from -100 to +100—the place constructive values mirror optimism, and unfavourable values point out pessimism.

With that out of the way in which, let’s begin.

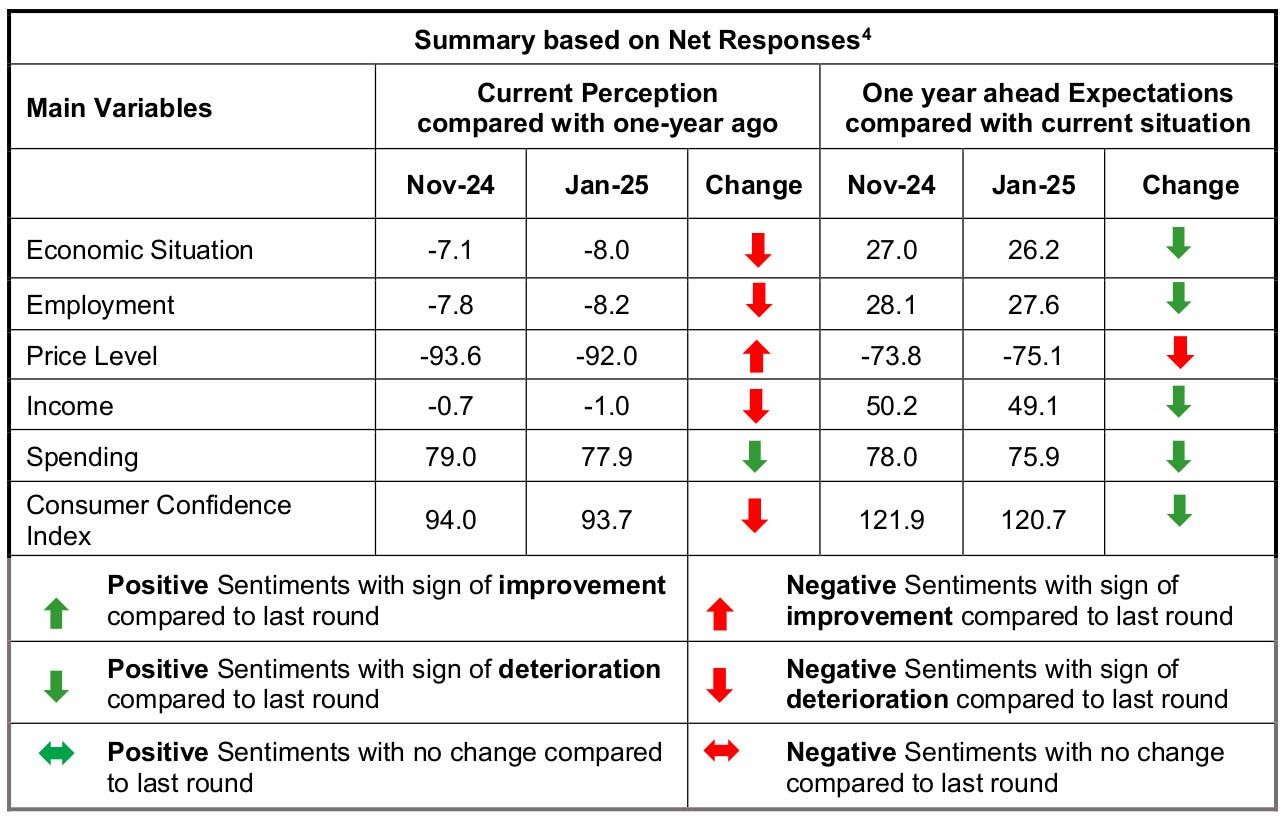

1. Client Confidence

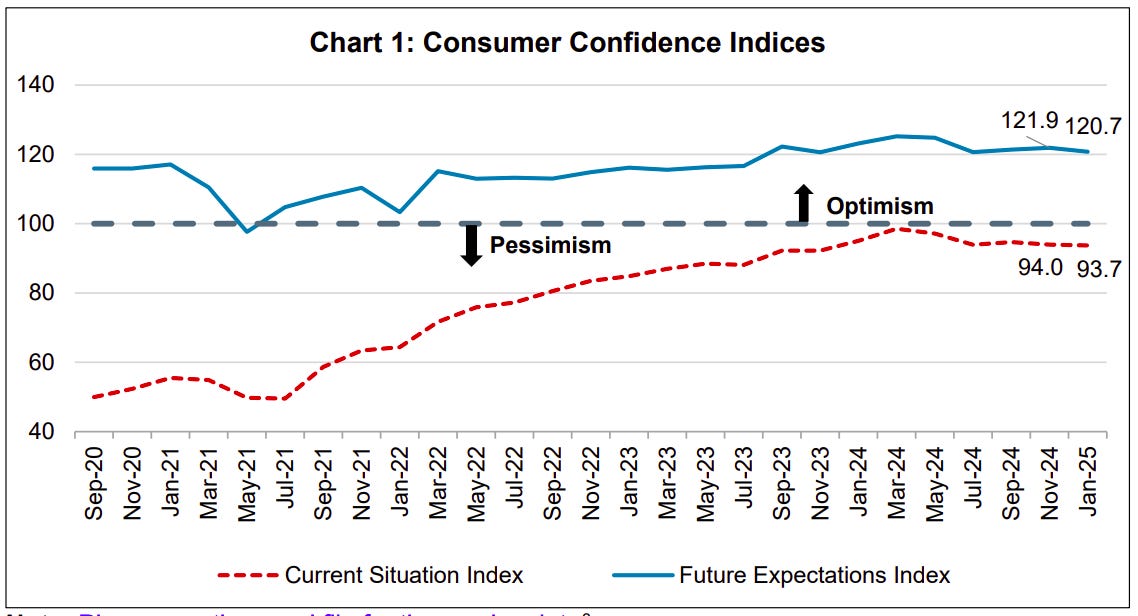

The Client Confidence Survey (CCS) helps perceive how individuals really feel concerning the economic system — each now and within the close to future. It tracks sentiment on jobs, earnings, inflation, spending, and total financial situations. It does so by surveying 6,000+ respondents throughout 19 main cities.

General, the January 2025 version of the survey reveals that individuals are a bit pessimistic about their present financial state of affairs, though they aren’t panicking simply but.

Supply: Client Confidence Survey

Supply: Client Confidence Survey

Diving deeper, listed below are the important thing takeaways from the most recent information:

Client confidence barely declined : Folks really feel barely worse concerning the economic system than earlier than. That mentioned, they nonetheless have excessive expectations for the longer term — believing that issues will enhance with time. Their optimism, nevertheless, has softened.

Employment sentiment weakened: Many respondents really feel like employment situations have deteriorated, whereas fewer individuals anticipate them to enhance. Employment sentiment jumped from -7.8 to -8.2.

Decrease pessimism on worth ranges, however inflation issues stay : Folks have lengthy been involved about worth ranges. These issues have eased barely, however households nonetheless anticipate inflation to rise within the coming 12 months. This might impression their spending habits.

Spending sentiment declined : Each important and non-essential spending sentiments dropped in January, in comparison with November 2024. That’s, individuals are much less inclined to spend than they had been a couple of months in the past. Future spending expectations nonetheless stay constructive — that’s, individuals nonetheless imagine that their spending will go up with time. Nevertheless, individuals are changing into extra cautious.

Earnings progress expectations dipped: Fewer households really feel that their earnings have improved, in comparison with previous durations. There may be much less certainty about future earnings positive aspects.

General, individuals have grow to be extra cautious concerning the economic system in the previous couple of months. Confidence is dipping, spending sentiment is softening, and earnings progress expectations aren’t nice. When individuals aren’t positive about their jobs and earnings, they maintain on to their cash as a substitute of spending it. That’s an issue. Non-public consumption makes up 60% of India’s GDP — so if individuals begin tightening their purse strings, progress takes successful. We’ve got clearly seen this play out within the final quarter.

Supply: ET

On the similar time, inflation expectations are rising. That is what we discovered within the IESH survey as nicely. In an ideal world, this could have led RBI to carry off on slicing rates of interest. However as progress fell, that possibility maybe wasn’t obtainable. We all know how that turned out.

The federal government, for its half, is making an attempt to show issues round. It is aware of sentiment is shaky, whereas consumption is down. That is how you must see its current bulletins. A private earnings tax minimize, adopted by a 25 bps repo price minimize? That’s the federal government saying loud and clear: “We see the issue, and we’re making an attempt to repair it. ”

Now, the massive query is: will individuals’s outlooks truly enhance? Or are these merely band-aid options? That’s what we’ll be watching within the months forward.

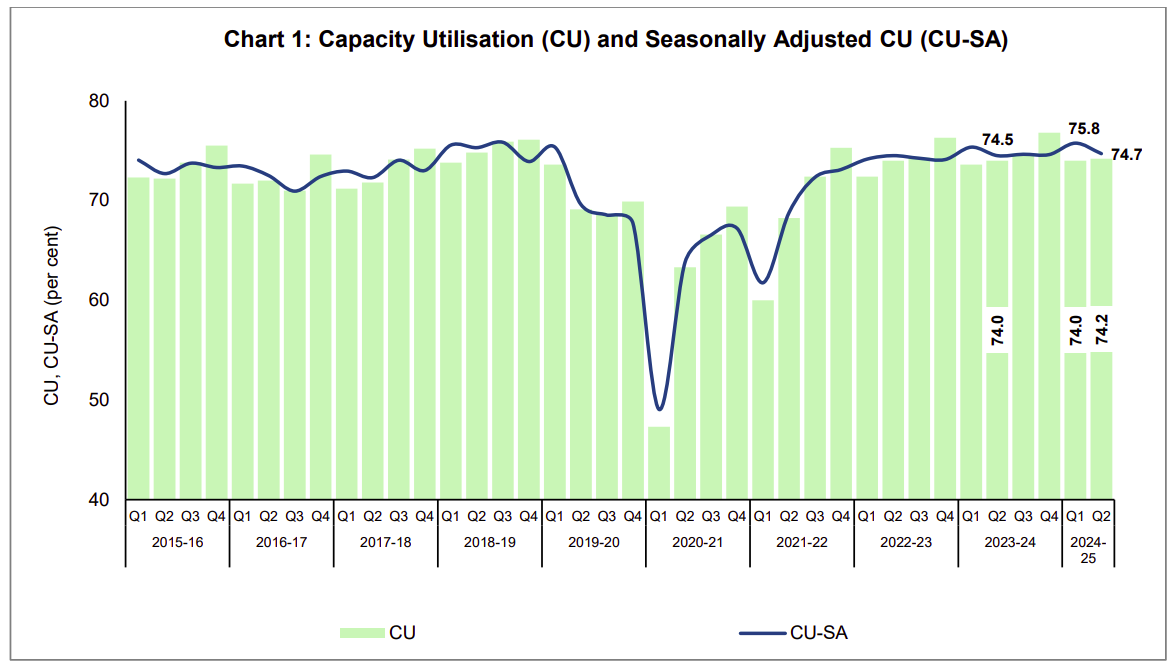

2. Manufacturing

To grasp the state of India’s manufacturing sector, we’ll have a look at insights from two key RBI surveys—the OBICUS Survey and the Industrial Outlook Survey. Whereas OBICUS focuses on producer’s order books, inventories, and capability utilization, the Industrial Outlook Survey captures enterprise sentiment, manufacturing traits, and price pressures. Collectively, they provide us a complete image of producing exercise and expectations, primarily based on the responses of 1,000+ manufacturing firms surveyed.

Listed here are our key takeaways from the most recent survey:

Manufacturing demand is holding up, however progress is sluggish: Corporations reported a slight improve in capability utilization — that’s, they’re working barely nearer to their peak capability. However there isn’t any marked distinction, indicating regular however not booming demand.

Supply: OBICUS Survey

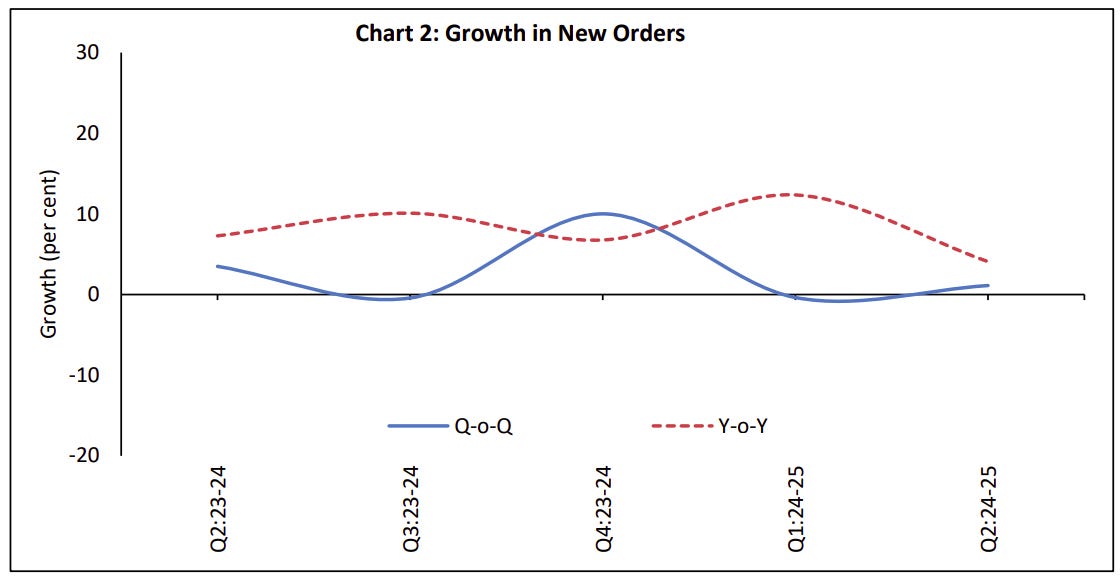

New orders are rising however at a slower tempo than earlier than. Whereas firms noticed sequential progress in orders, year-on-year progress has come down, suggesting some slowdown:

Supply: OBICUS Survey

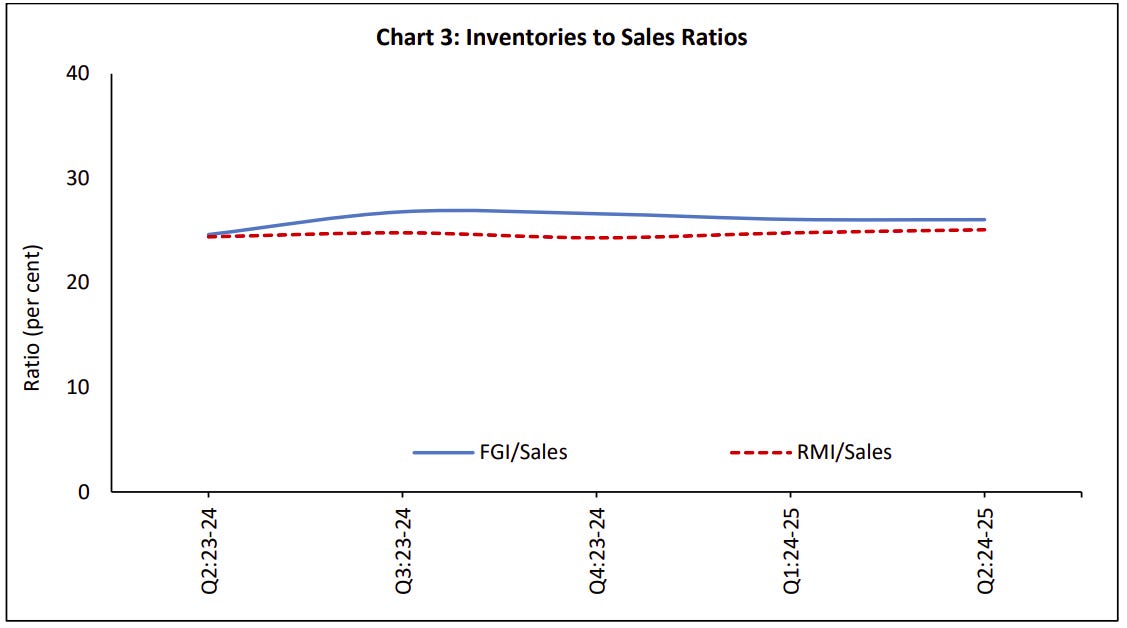

Inventories stay secure. Producers should not overstocked, that means they’re producing simply sufficient to satisfy demand. There’s no noticeable ramp-up of their manufacturing, nevertheless:

Supply: OBICUS Survey

Enter prices are rising, squeezing margins. Corporations are scuffling with greater uncooked materials prices. Whereas they’re passing a few of these prices on to clients by way of worth hikes, revenue margins stay below strain. To present you some numbers, the price of uncooked supplies elevated from 38.7 to 46.5 within the final quarter. This can be a unhealthy signal. On the similar time, promoting costs additionally went up, from 0.2 to 2.6, which implies firms are charging extra for his or her merchandise. That mentioned, they aren’t capable of move on all the improve of their prices. Because of this, margins dipped from -10.2 to -12.8.

Supply: Industrial Outlook Survey

In all, manufacturing is actually not in a stoop. Nevertheless, it’s not firing on all cylinders both. Demand is regular, however not surging, and rising prices are a rising concern.

If enter costs keep excessive however demand doesn’t choose up considerably, producers would possibly maintain again on enlargement. Capability utilization, too, is stagnant, which signifies that there’s no need, at an combination degree, for extra manufacturing capability. If this pattern continues, India’s decade-long malaise of below-par non-public investments will keep it up, hurting total financial progress.

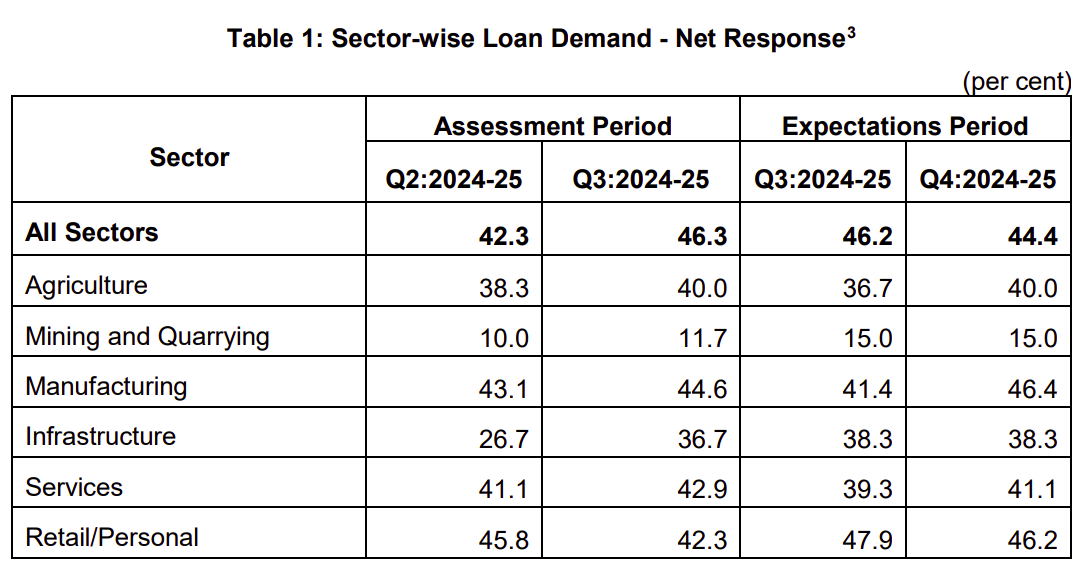

3. Financial institution Lending: What the Survey Reveals

The Financial institution Lending Survey (BLS) provides us a snapshot of the sentiment of borrowing amongst companies and people. It additionally seems to be at whether or not banks are making it simpler or more durable to get loans. This survey captures the views of senior mortgage officers from 30 scheduled business banks (i.e. 90% of India’s SCBs), offering insights into credit score demand, lending situations, and future expectations.

Listed here are the important thing takeaways from the most recent survey:

Mortgage demand has grown throughout most sectors, notably manufacturing, infrastructure, and companies. This means that companies are nonetheless increasing and investing. However, retail and private mortgage demand has slowed down. You’ll be able to interpret this in multiple means. For example, customers could also be extra cautious about taking up debt, presumably attributable to job issues or rising residing prices. On the similar time, the RBI has elevated threat weights on banks for unsecured client loans, making them dearer for debtors. Because of this, the demand for such loans might have taken successful.

Supply: Financial institution Lending Survey

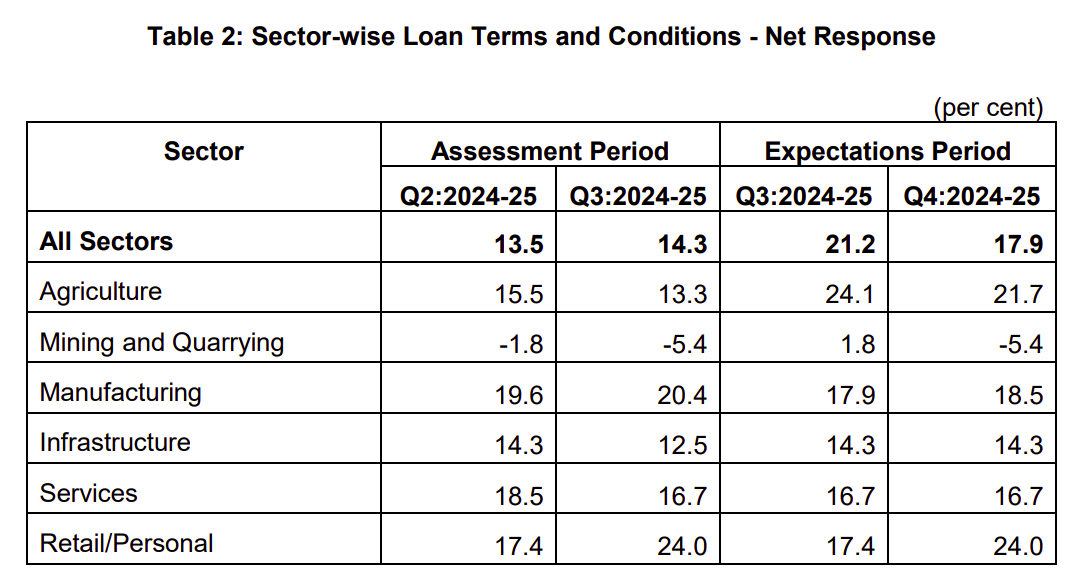

Lending phrases stay simple in most sectors, aside from mining, the place situations have tightened. It’s potential that banks are seeing greater dangers on this sector and are pulling again. Surprisingly, in comparison with the final quarter, getting a private mortgage has grow to be a lot simpler, as phrases and situations have eased — even because the demand for them has taken successful.

Supply: Financial institution Lending Survey

Banks anticipate mortgage demand to melt barely within the subsequent quarter, reflecting a short lived dip relatively than a long-term slowdown. Credit score progress continues to be intact, that means companies have entry to funding, however client borrowing is slowing down—a pattern that would impression spending and financial momentum within the months forward.

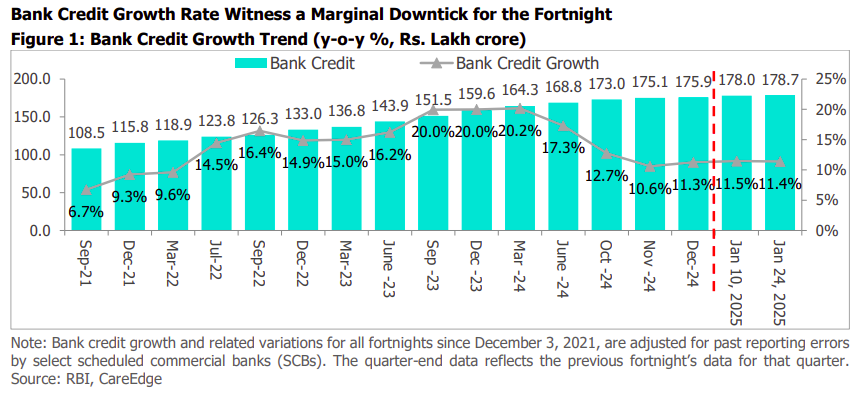

Now, these findings echo the Fortnightly Credit score and Deposit Replace by Care Edge.

The BLS means that mortgage demand was rising however displaying indicators of moderation, particularly in retail/private loans. The Fortnightly Replace confirms this pattern. Since November, credit score progress has slowed from final 12 months’s peak of over 20% progress and now stands at 11.4%. This aligns with banks’ expectations of slower mortgage demand in upcoming quarters.

Supply: Care Edge

The RBI surveys present that individuals are getting cautious concerning the economic system. Client confidence is dipping, manufacturing is regular however not booming, and companies are nonetheless borrowing, however private loans are slowing. With inflation worries, progress may decelerate, making coverage help extra vital than ever.

Between April 1 and February 10 of FY25, India’s internet direct tax collections rose by 14.7% to ₹17.8 Lakh Cr., pushed by a pointy 20.9% progress in non-corporate tax collections, totaling ₹9.4 Lakh Cr. Company tax collections grew at a slower tempo of 6.1%, reaching ₹7.8 Lakh Cr. Securities Transaction Tax (STT) noticed a notable spike of 65.05%, amounting to ₹49,201 crore, reflecting heightened inventory market exercise.

Lam Analysis, a number one U.S. semiconductor tools producer, is about to take a position over $1.2 bn in Karnataka, marking a big step in India’s semiconductor ambitions. The MoU signed with the Karnataka Industrial Space Improvement Board is a part of India’s bigger $10 billion incentive bundle geared toward constructing a strong semiconductor ecosystem. The Indian semiconductor market is projected to the touch $63 billion by 2026, and Lam’s entry will speed up this progress.

Gold leasing charges in India have doubled inside a month, reaching file ranges as international provide tightens. Sometimes ranging between 1.5% to three%, these charges have surged nicely past the norm, considerably rising prices for jewellers like Titan, Kalyan Jewellers, and Tribhovandas Bhimji Zaveri. The surge stems from international bullion banks diverting gold to the U.S., the place futures commerce at a $28 per ounce premium over spot costs.

This version of the e-newsletter was written by Krishna and Kashish

Have you ever checked out One Factor We Realized?

Have you ever checked out One Factor We Realized?

It’s a brand new side-project by our writing group, and even when we are saying so ourselves, it’s fascinating in a bizarre however great means. Daily, we chase a random fascination of ours and write about it. That’s all. It’s chaotic, it’s unpolished – nevertheless it’s sincere.

Thus far, we’ve written about all the pieces from India’s state capability to toilet singing to protein, to Russian Gulags, as to whether AI will kill us all. Test it out for those who’re in search of an enchanting new rabbit gap to go down!

Subscribe to Aftermarket Report, a e-newsletter the place we do a fast day by day wrap-up of what occurred within the markets—each in India and globally.

Thanks for studying. Do share this with your mates and make them as good as you might be ![]() Be part of the dialogue on at the moment’s version right here.

Be part of the dialogue on at the moment’s version right here.