Our purpose with The Every day Temporary is to simplify the most important tales within the Indian markets and make it easier to perceive what they imply. We gained’t simply let you know what occurred, however why and the way too. We do that present in each codecs: video and audio. This piece curates the tales that we discuss.

You may hearken to the podcast on Spotify, Apple Podcasts, or wherever you get your podcasts and watch the movies on YouTube. You can even watch The Every day Temporary in Hindi.

In at the moment’s version of The Every day Temporary:

Behind the Pharma Rep Ban Saga

India’s Tyre Giants Navigate a Bumpy Trip

The Indian Pharmaceutical Alliance (IPA) and the Directorate Basic of Well being Providers (DGHS) are locking horns over a brand new rule: which bans medical representatives (MRs) from authorities hospital premises.

In plain phrases, the Well being Ministry (by way of DGHS) advised all central authorities hospitals, “No pharma gross sales reps allowed inside, interval .” The thought is to cease any interference with affected person care – representatives can not hold round clinics, pitch medication, or affect prescriptions whereas sufferers wait in line.

As you would possibly anticipate, the IPA — a foyer of massive home drug corporations — isn’t glad. They’ve known as this a ‘’blanket ban**’** that would do extra hurt than good, and are urging the federal government to suppose once more.

We’re right here to unpack why this tussle is occurring, what’s at stake, and what it means for docs, sufferers, and the pharma business.

Who’re MRs, and why do pharma corporations want them?

Medical representatives (MRs) are form of a giant deal for the pharma business. They play a dual-role: half educator , half salesperson . An MR’s job is to go to docs — armed with brochures and drug samples — and inform them in regards to the newest medication or remedies their firm gives.

For instance, if an organization simply launched a brand new blood stress capsule, their MR will drop by a hospital to speak with cardiologists about why this capsule is nice. Subsequent time the physician writes a prescription, this would possibly simply nudge them to recollect the capsule.

This isn’t essentially a foul factor. So long as pharma corporations are principled, in idea , everybody advantages when docs are updated on remedies. In follow, nonetheless, the truth that these interactions double as advertising alternatives for pharma corporations can create issues.

Basically, when an MR builds a relationship with docs, that may be a double edged sword. Whereas they may present real medical updates to docs, in much less scrupulous circumstances, they may have an effect on the medical judgement of a health care provider with the freebies and perks they provide, inducing them to decide on their drug, even when it isn’t the only option for the affected person. They’re basically straddling a high-quality line between schooling and promotion .

There are ethics at stake

The large fear, right here, is what occurs when revenue takes priority over affected person curiosity. If a health care provider prescribes a drugs solely as a result of an MR supplied them a candy perk — say a flowery dinner — that’s a significant issue. It may imply sufferers find yourself with pricier or less-suitable medication, all due to invisible stress on the physician.

Well being authorities and watchdogs worry that with out guidelines to ban such behaviour, MRs may flip hospital corridors into bazaars of affect. For this reason there are moral codes in place around the globe to maintain pharma advertising in examine. In america, pharma corporations observe the PhRMA Code – tips that equally ban giving out something that isn’t primarily for affected person profit. Europe has the EFPIA Code of Apply, which does the identical for EU international locations.

Basically, these codes draw a transparent line: Share information? Sure . Throw cash or items at docs? No . They exist to ensure that when your physician prescribes one thing, it’s since you want it – not as a result of a salesman requested them to.

Equally, India has the ‘Uniform Code of Pharmaceutical Advertising and marketing Practices’ (UCPMP), first launched in 2015 as a set of do’s and don’ts for drug advertising. It mainly tells pharma corporations to not bribe docs with lavish items, journey junkets, or goodies – preserving it skilled and informative.

You understand what’s humorous, although? For years, UCPMP was voluntary . It was extra of a gentleman’s settlement than a regulation. Basically, pharma corporations had the selection to not be unethical in how they approached docs.

New code, new ban, and business pushback

To additional clear up these practices, the Indian authorities up to date the UCPMP in early 2024 — giving it extra tooth. What was as soon as completely voluntary was now given a “quasi-statutory” standing. The code now formally utilized to pharma associations and firms, and an oversight committee was put in place as a watchdog. The up to date code banned apparent freebies, like sponsored overseas junkets, luxurious resort stays, or private items.

However then, the Well being Ministry went even additional. In its newest transfer, it handed an outright ban on MRs from coming into central authorities hospitals. In late Might 2025, the DGHS issued a round to all these hospitals — in essence asking them to not give entry to any medical representatives. Any info they wanted to share might be despatched over electronic mail, or by means of different digital channels.

The federal government wished to point a ‘zero tolerance’ coverage in the direction of medical representatives. Having drug reps popping into wards and OPDs was inflicting disruption — docs’ time was being eaten up, sufferers had been stored ready, and there was potential for “ undue affect ” on prescriptions. And so, they might be banned outright. Any info they wanted to share might be despatched over electronic mail.

The IPA shortly raised its voice in protest. The alliance argued that the ban overshot its mark. Even when there was a case that these representatives ought to keep self-discipline, they shouldn’t shut out interactions fully . In a letter to the Well being Ministry, the IPA harassed that MRs really serve a ‘ essential instructional function**’** in healthcare. A blanket ban, it warned, may “impression the expansion of the pharmaceutical sector” and result in job losses for 1000’s of MRs.

As an alternative, they urged a compromise: enable MRs in, however create a construction round their visits: like setting particular days or hours for these interactions, in order that they don’t interrupt clinics.

Loopholes, grey areas, and why the coverage won’t stick

Right here’s the place issues get difficult: On paper, banning MRs from hospitals and imposing advertising codes sounds nice. In follow, they arrive with main weak spots:

Enforcement stays a problem: Our parliament itself hasn’t handed a regulation on pharmaceutical advertising. The UCPMP nonetheless isn’t regulation — it’s functionally only a authorities round. Its “quasi-statutory” means it’s form of enforceable, however its scope is restricted. It doesn’t have a robust monitoring mechanism, or a regulator that may prescribe heavy penalties. Its enforcement nonetheless depends on business our bodies policing themselves.

It’s not the primary time: This isn’t the primary time the federal government has tried to curb MRs in hospitals. A really comparable order additionally went out in 2023 — basically telling central hospitals to fully curtail MR visits, whereas info on new therapies must be despatched by way of electronic mail. The actual fact that we’re once more seeing the identical directive in 2025 suggests the 2023 order was largely ignored.

Different kinds of measures have failed too: There’s already a rule (courting again years by way of the Medical Council of India, now NMC) that authorities docs should prescribe medicines by their generic title, not by model. In idea, this could have solved the issue already. For example, if a health care provider can solely write one thing like “ibuprofen 400mg” as a substitute of a particular model to search for, they couldn’t probably present bias towards anyone firm. Solely, enforcement of this rule, too, has been patchy. Authorities docs caught pushing manufacturers may technically face motion, however in actuality, this seldom occurs.

Digital affect is affect too: Banning bodily visits by reps doesn’t eradicate pharma affect. It merely adjustments the channel by means of which docs are influenced. The 2025 directive itself acknowledges that MRs can nonetheless share data digitally — by way of emails, Zoom calls, or WhatsApp teams. And that’s exactly what they’re doing. The truth is, modes of digital promotion are slowly turning into increasingly outstanding, as per a current examine.

Supply

Affect, in brief, finds a manner. The taking part in subject could shift, however the sport of getting a health care provider’s consideration isn’t going to fade.

Due to all of this, some see the ban as extra performative than sensible . It’s a daring announcement, it’s arduous to really implement. With out robust follow-through, each the UCPMP tips and the hospital rep ban may find yourself as well-intentioned memos that collect mud, whereas the true dynamics of drug promotion proceed with a number of tweaks.

However there’s yet another factor: all of this could be moreover the purpose .

Why entry issues extra

We spoke to a couple people within the business whereas attempting to grasp this story. And that gave us a very totally different perspective on this: in terms of authorities hospitals, the presence or absence of MRs won’t matter an excessive amount of anyway. The supply of medicines in such hospitals runs on a very totally different system, in any case.

Authorities hospitals sometimes procure their medicines by means of a young system. Basically, they invite bids for medication — based mostly on the chemical , as a substitute of the model . These purchases are made in bulk from whichever firm gives one of the best worth whereas assembly high quality requirements. Meaning for every drugs (say, paracetamol), the hospital would possibly inventory one or two chosen manufacturers that gained the availability contract. These medication are then given free or at very low value to sufferers by way of the hospital pharmacy / dispensary.

Now, we aren’t saying no person tries to sport this method: solely that sending MRs to docs would do little on this regard.

If a health care provider in a public hospital writes a prescription, they often both use the generic title or the title of no matter model is stocked in-house for that drugs. Most sufferers at these hospitals will get the drugs proper there, freed from cost.

Take into account what which means for an MR: If their firm’s model isn’t the one the hospital shares, no quantity of schmoozing with docs will get sufferers that model – it’s merely not out there within the constructing.

Firms know this. There’s little level in closely advertising a model to docs if their hospital doesn’t inventory it. If a authorities hospital solely carries ABC’s diabetes drug, for example (as a result of ABC gained the tender), an MR from XYZ Co. would possibly attempt to promote their model — however it could make no sense. Docs merely can’t prescribe it for in-hospital use. Poorer sufferers that depend on free medicines are unlikely to go outdoors and purchase a distinct model. The truth is, our supply advised us that many pharma corporations don’t even trouble sending reps to some authorities hospitals in the event that they aren’t suppliers there. It’s not well worth the effort.

What this implies is that the place public hospitals are involved, entry and availability trump promotion. Pharma corporations make their cash on the level of procurement , not prescription . If a pharma firm desires its drug used there, successful the tender or getting on the hospital’s formulary is the true prize – not chatting up docs.

The bottomline

On the finish of the day, this back-and-forth between the federal government and the pharma business feels a bit like working in circles.

The federal government is banning one thing that, in idea, it already banned earlier than and arguably can’t absolutely police. The IPA is pushing again to guard a follow which may not be as essential in authorities settings as they declare. Each side insist they’ve affected person curiosity at coronary heart – the federal government cites ethics and unclogging hospital hallways, whereas pharma corporations discuss preserving docs knowledgeable for higher affected person care.

To us, although, it appears like either side are speaking previous one another.

The core points, in the meantime, stay in limbo: How can we guarantee docs get unbiased info on new remedies? How can we implement moral advertising with out actual authorized tooth? How can we be sure that sufferers, particularly in public hospitals, get one of the best medicines with out hidden business agendas creeping in?

Sadly, for this story, now we have extra questions than solutions.

There’s one thing brutal in regards to the tyre enterprise.

This can be a sector that we checked out for the primary time, and we discovered it extraordinarily fascinating. And that’s due to simply how dependent these companies are on what’s taking place outdoors. See, in case you’re a tyre producer, your two greatest value inputs — pure rubber and crude oil derivatives — can swing by as a lot as 30% in worth in only a few months. You are able to do nothing to regulate that, in need of some sensible hedging. You’re additionally taking part in second fiddle in an business the place automotive producers, and never tyre producers, name the photographs.

And but, you’re anticipated to make decade-long bets on manufacturing facility areas, expertise platforms, and market positioning that can decide whether or not your organization thrives or struggles for years to come back.

This basic rigidity defines India’s ₹90,000+ crore tyre business turnover. Firms should navigate quarterly commodity worth shocks whereas concurrently making huge strategic selections about the way forward for Indian mobility. Do you wager large on electrical automobile tyres when EVs are nonetheless beneath 2% of gross sales? Do you have to make investments closely in truck radials when international freight demand is flagging? Are you able to double down on exports in an period when commerce insurance policies can change in a single day?

The attention-grabbing half isn’t simply that these corporations face this problem — it’s how in a different way every main participant is selecting to navigate it. Whereas all of them make tyres, they’re basically making very totally different bets about what Indian transportation will appear like in 2030. And people selections are already displaying up of their outcomes.

What’s taking place within the tyre business

Earlier than we go into the person corporations, let’s set some context.

The tyre enterprise is especially difficult due to simply what number of essential elements lie fully outdoors administration management, and but could make or break annual efficiency. Listed here are simply a few of what the business is seeing:

The uncooked materials roulette

Tyres companies are closely depending on commodity costs . 80-85% of a tyre’s uncooked materials prices come from pure rubber, artificial rubber, carbon black, and metal wire.

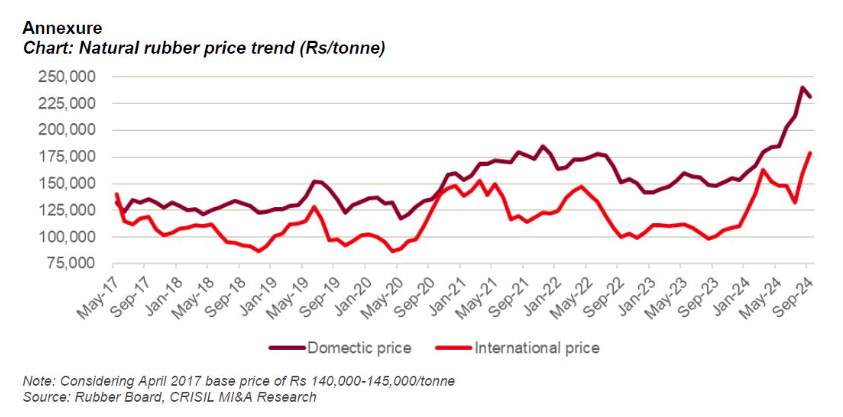

Rubber, particularly, is a giant deal. If you need a quick-and-dirty metric to trace this sector, take a look at pure rubber costs in Kerala, and also you’ll get an excellent sense of the place its margins could be. That stated, Kerala alone can’t produce sufficient rubber to feed the business. India produces solely ~800,000 tonnes of pure rubber in opposition to the consumption of ~1.3 million tonnes. Meaning the tyre business’s destiny is pushed, to an important diploma, by international rubber costs.

Not too long ago, this grew to become a significant challenge for the business. In late 2024, rubber costs all of the sudden rose by 33% to cross ₹200 per kg for the primary time in a decade. Inside a single quarter, tyre firm margins noticed horrible stress. You may see the impression of this spike clearly of their outcomes, with most of them seeing margins fall.

Supply

The business’s many temper swings

Tyre corporations don’t have a major market of their very own. 30% of their enterprise comes from new automobile fitment, which is straight depending on the plans of automotive corporations. And so, tyre corporations continually attempt to predict and journey the automotive business’s cycles. This makes the enterprise uniquely tough to handle.

The opposite 70% of tyre income comes from substitute demand, which is inherently unpredictable. That will depend on how lengthy tyres final in real-world situations — one thing influenced by every part from utilization patterns, to highway high quality, to climate. Completely different corporations would possibly take a look at totally different dynamics to run their enterprise. For example, whereas JK Tyre, with its heavy business automobile focus, is extra delicate to freight and infrastructure cycles. CEAT, robust in two-wheelers, correlates with gas costs and concrete mobility patterns.

These days, there’s a brand new sport these corporations should play. As individuals transition to electrical automobiles, they should develop completely new tyre applied sciences. In any case, EVs are heavier, quieter, and ship instantaneous torque. However the query is: how do you intend investments into EVs? In any case, EVs nonetheless signify a small fraction of automotive gross sales at the moment, and it’s arduous to foretell when adoption will speed up. Unhealthy timing, right here, may harm an organization’s prospects.

Tyre protectionism

India’s regulatory regime does quite a bit to form the business.

In June 2020, India moved tyres to the “restricted” import class. Successfully, corporations now require licenses for tyre imports. Till this level, Chinese language tyres had captured 12-15% of India’s substitute market pre-2020. However this coverage insulated our market, defending India’s home tyre producers from low-cost Chinese language imports. We additionally positioned anti-dumping duties on Chinese language truck and bus tyres, serving to our home business nook the market even additional.

On the identical time, although, the federal government has additionally made Indian tyres costly, which may lower down demand. The GST fee on tyres is 28%, making substitute tyres costly. Customers, in consequence, are pushed to delay tyre adjustments. This can be a security concern that the business continues lobbying in opposition to.

4 corporations, 4 strategic approaches

To grasp how India’s tyre sector is dealing with this complexity, we picked 4 corporations that collectively management 70-75% of the market. Every represents a distinct strategic strategy to the business.

There’s MRF, the undisputed king with almost 30% market share, constructed on dominating India’s home substitute market.

Apollo Tyres is a world sophisticate, producing important income from Europe by means of a genuinely worldwide manufacturing presence.

JK Tyre is a business automobile specialist, with most of its 15% market share coming from truck and bus tyres.

CEAT is the innovation-focused challenger, which is pushing up its 10-15% market share with Trade 4.0 manufacturing and sensible tyre applied sciences.

Collectively, these 4 supply totally different solutions to the identical basic query: how do you anticipate and survive India’s quickly evolving mobility panorama?

MRF: The Fortress India Technique

MRF, arguably India’s tyre incumbent, has basically constructed itself a robust home fortress. The corporate operates 9 vegetation throughout India and might pump out 85 million tyres yearly. Greater than 90% of its income comes from home gross sales. It depends on the nation’s largest supplier community for the job — with 5,000+ devoted sellers — and it maybe has the strongest model fairness in substitute markets.

Final quarter was a fairly robust one for the corporate. MRF closed This fall with a income of ₹7,075 crore — up 11% year-on-year. Of this, ₹512 crore got here to the corporate as its internet revenue, a rebound of 29% from the earlier quarter. Over the total 12 months, MRF crossed ₹25,000 crore in income whereas sustaining stable profitability.

Sadly, we’re flying barely blind whereas attempting to decode MRF’s enterprise. Whereas its rivals rolled out elaborate investor shows with vibrant charts and graphics, after which adopted these up with prolonged investor calls, from what we will see, MRF did none of that this quarter. It simply put out the uncooked numbers and little else.

For those who’ve come throughout any administration commentary, although, tell us within the feedback!

That stated, right here’s what we will inform.

Impressively, MRF stored profitability excessive this 12 months regardless of rubber costs leaping by over 33% over the 12 months. Maybe due to MRF’s premium positioning, it weathered this storm higher than its friends.

From what we will inform, the corporate isn’t considering of reinventing itself or altering its enterprise very considerably. The corporate is doubling down on what they do finest — increasing home capability and sustaining its efficiency testing capabilities. Their ₹4,500 crore funding in a brand new plant in Gujarat indicators this continuity — whereas the corporate is increasing its manufacturing base outdoors South India, its core operations stay the identical. India’s market is large enough to maintain targeted progress, they imagine, and by catering to home substitute demand, they will maintain on to the place they’re.

Though MRF not too long ago started catering to electrical automobiles as properly, this presence is pretty nascent in the mean time. It even appears to be ready to see which EV segments take off earlier than committing fully to the phase.

Apollo Tyres: The worldwide integration play

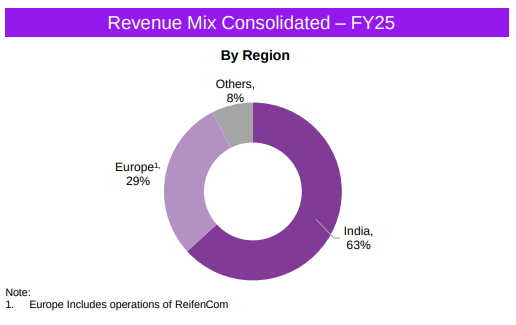

In distinction to MRF, Apollo isn’t fixated on the Indian market. It has a ‘dual-continent’ strategy — its enterprise is cut up between India and Europe, permitting them to serve premium European markets with native manufacturing, whereas leveraging Indian value benefits to succeed in rising markets.

Thoughts you, Apollo isn’t simply exporting to Europe; they’ve a genuinely worldwide manufacturing presence. Past its 5 vegetation in India, the corporate runs two vegetation in Europe — within the Netherlands and Hungary. 63% of its income comes from India, whereas 29% is available in from Europe.

Supply

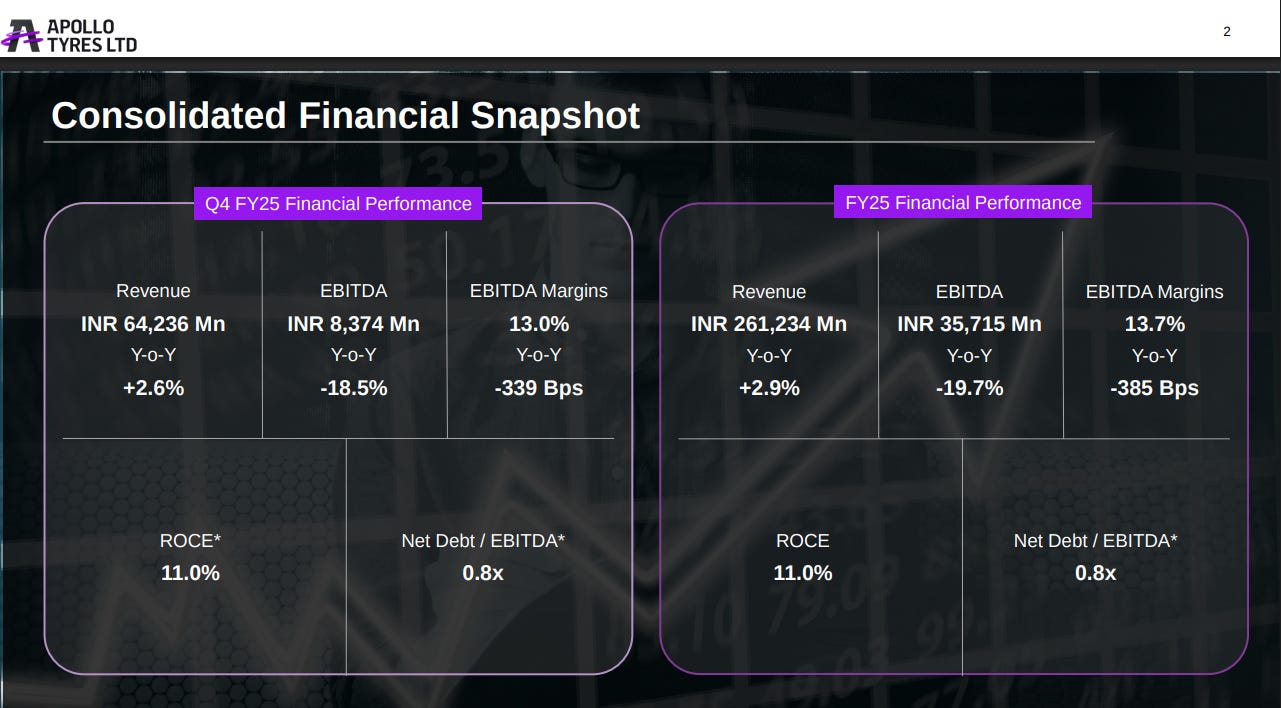

Not too long ago, the corporate’s efficiency has been decidedly subdued. Apollo noticed a This fall income of ₹6,424 crore, with a internet revenue of ~₹185 crore. This is a bit more than half its ₹354 crore revenue in the identical quarter final 12 months. For FY 2024-25, Apollo’s income grew barely, by 3%, to ₹26,123 crore. Its profitability took a success, nonetheless, with annual earnings falling from ₹1,722 crore to ₹1,121 crore — largely as a result of its prices shot up.

Supply

Apollo candidly acknowledged its below-average efficiency in its earnings name. In line with its Managing Director, Neeraj Kanwar:

“So like I discussed to you, sure, this 12 months has been very, very difficult. We’ve underperformed, however the inexperienced gentle is that now we have put numerous initiatives within the subject.”

What held it again?

There are some things that Apollo was shuffling round this quarter. For one, the corporate pulled again its low-margin OEM enterprise. It additionally confronted capability constraints in Hungary, which impacted European volumes. Most curiously, although, the corporate spent a while reorienting itself. It shifted from what it described as a ‘regional’ to a ‘international’ working mannequin — one thing that was a very long time coming. If that evaluation is true, this underperformance may simply be a slight hiccup.

“We’ve restructured within the month of Might, June, the place we went from being a regional firm to extra international. And it has taken us time. And that’s why possibly one of many causes for the underperformance is there.”

Elsewhere, Apollo has made a number of strikes. It was first amongst its friends to come back out with EV-specific tyres, for example. It got here out with its ‘Amperion’ vary for vehicles and ‘WAV’ for two-wheelers — incomes a 5-star gas effectivity score. Whereas that is partly to remain related in Europe, which is much forward of India in shifting to EVs, Apollo additionally appears to have an extended wager that city India will undertake EVs.

That is additionally evident in its strategy to innovation. Apollo has been investing in twin R&D centres — in Chennai and the Netherlands — to bridge European expertise with India’s manufacturing economics. If this wager works out, it may compete with international gamers on expertise and high quality, and never simply worth alone.

All in all, Apollo’s quarterly efficiency has been sub-par, nevertheless it factors to some causes for hope subsequent time round:

“now we have not too long ago employed a chief provide chain officer. He’s Indian, coming from a really giant German firm. We’ve not too long ago employed Rajeev Kumar Sinha, who has come as a chief of producing, who comes with an experience of Cipla for the previous 9 years. So, these are the 2 new joinees which have are available in. And with that, it does take time for individuals to settle in and to begin performing.

So, like I stated in my earlier reply, Q1 goes to be our quarter. Hopefully, we are going to come again with double digit progress.”

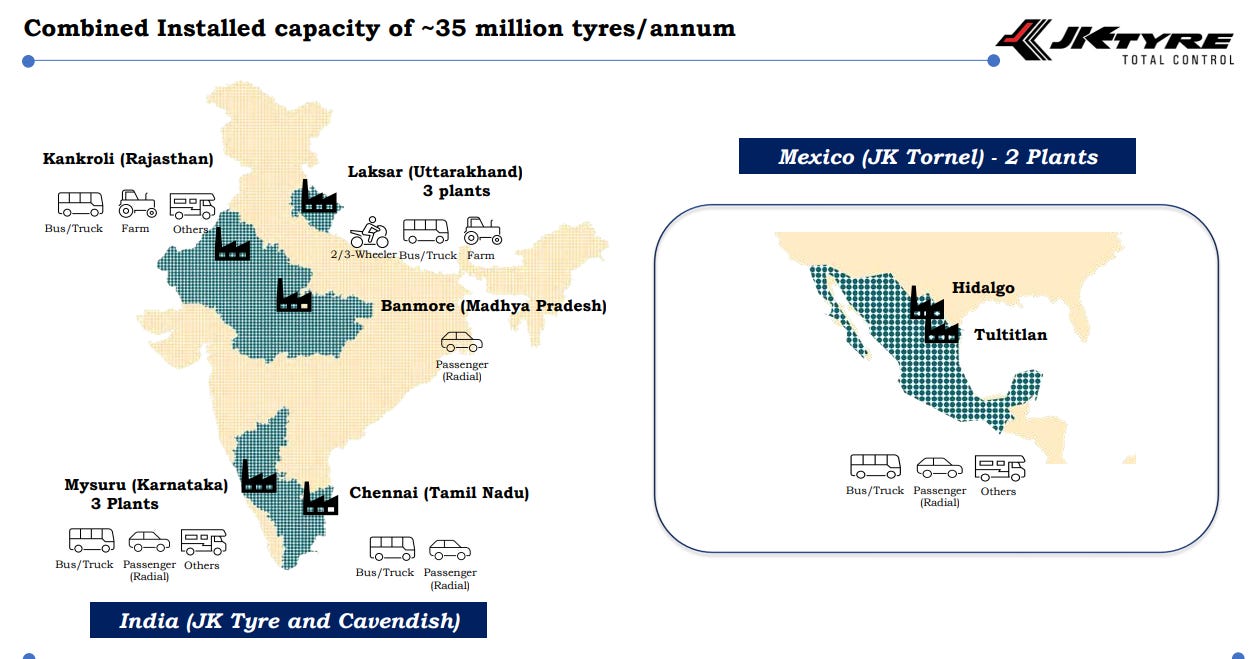

JK Tyre: The Americas bridge technique

JK Tyres has positioned itself very in a different way from both MRF or Apollo: it’s a business automobile specialist. The truth is, JK Tyre was amongst India’s first corporations to supply truck radials.

Like Apollo, JK Tyres has diversified its geographic market too: serving India and the Americas concurrently. The corporate operates eleven manufacturing vegetation, and whereas 9 are in India, two of these, housed beneath the JK Tornel model, are in Mexico . This offers JK Tyre a novel bridge to markets throughout the Americas.

For this reason it has such a formidable export presence. The corporate exports to over 100 international locations and has specialised in giving international market entry to cost-effective Indian manufacturing.

Supply

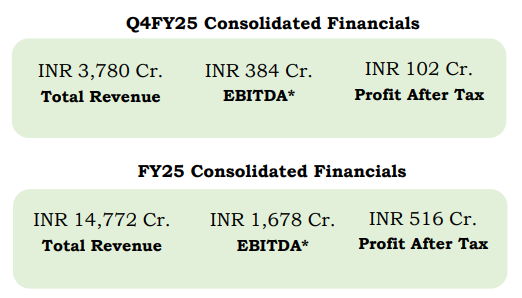

Extra instantly, the quarter passed by, for JK Tyre, was a dismal one. It reported This fall income of ₹3,780 crore with internet revenue of ₹102 crore, down about 31.4% year-on-year. The quarter that got here earlier than was even worse — earnings had plunged 62% because of rubber worth spikes. It recovered considerably from these lows by year-end. Its full-year income, finally, was roughly ₹14,772 crore.

Supply

Trying forward, although, JK Tyre believes it’s heading into FY26 with an optimistic demand outlook — particularly for tyre replacements and exports. However its numbers won’t look too good. The corporate’s sitting on notably costly inventories, and that would make it look much less worthwhile. As the corporate stated on its earnings name:

“In Q1 and Q2, we had taken some strategic stocking of the fabric which helped us to evade a number of the value in Q2. However then that strategic stock had depleted and Q3 noticed the total impression of the uncooked materials. Sure, there was a significant impression on EBITDA margins because of larger uncooked materials value in Q3. It’s solely within the quick time period — the working capital borrowings have gone up within the final 9 months interval and that is to keep up the strategic stock and in addition some completed items stock had been accrued. However that is going to get corrected in subsequent one or two quarters.”

The corporate’s capability utilisation is reasonably excessive, particularly in passenger automotive radials. If it desires to develop its volumes, it should give attention to shortly commissioning upcoming enlargement tasks. Moreover, the agency’s Mexico operations face overseas alternate headwinds, although administration plans to spice up exports to North America to offset native softness.

The corporate is exploring EV functions for business automobiles and has been engaged on sensible tyre applied sciences and premium materials functions for its business automobile focus. Their wager: business automobile progress and export markets will drive long-term worth, leveraging their early experience in truck radials.

CEAT: The Good Manufacturing Wager

CEAT is an organization constructed round a give attention to manufacturing excellence reasonably than scale. It does have first rate scale — the corporate operates six vegetation in India, producing 41+ million tyres yearly. Their Chennai plant (opened 2020) was designed from the bottom up for passenger automotive and two-wheeler radials, focusing on OEM clients like Hyundai and Kia.

CEAT delivered a robust quarter this March, regardless of taking a small dent to its profitability. CEAT managed This fall income of ₹3,421 crore — up 14.3% year-on-year. Its internet revenue for the quarter fell marginally, nonetheless, from ₹102.3 crore to ₹98.7 crore. The complete 12 months noticed income progress of 10.7% to ₹13,218 crore, although annual revenue dropped to ₹471 crore from ₹635 crore final 12 months, as its margins fell.

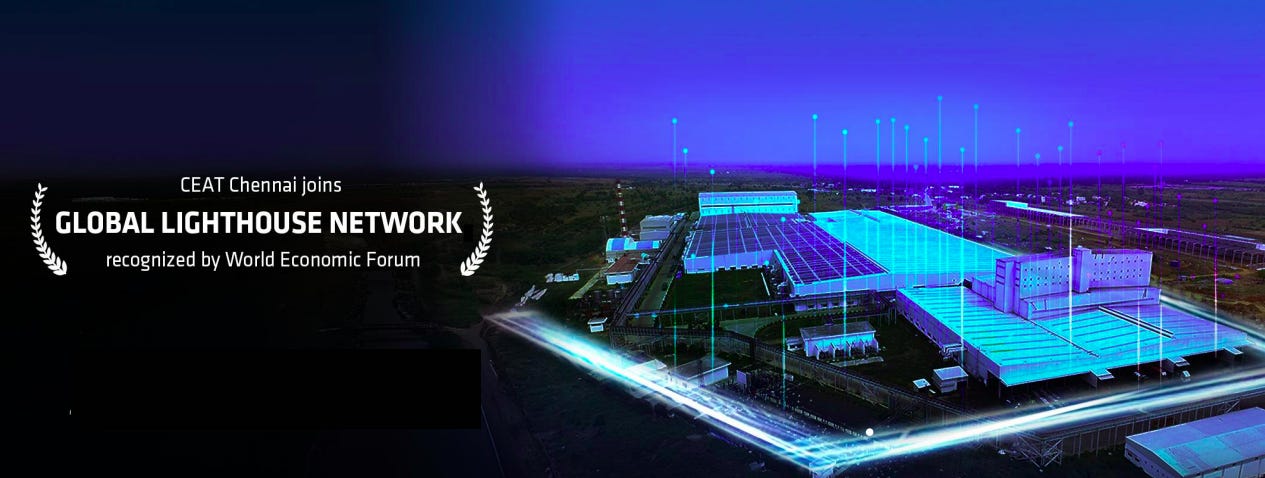

Elsewhere, although, there was extra thrilling information for the corporate. CEAT grew to become the primary tyre firm globally to obtain the World Financial Discussion board’s “Lighthouse” certification. Each its Halol and Chennai vegetation had been inducted into the ‘International Lighthouse Community’ — a recognition that it was utilizing ‘Trade 4.0’ applied sciences like superior analytics, machine studying, and predictive upkeep.

Supply

By means of this expertise push, CEAT’s attempting to compete with international giants on their very own turf. It’s basically betting that superior manufacturing and innovation can overcome scale disadvantages, permitting them to punch above their weight, in an business the place greater has historically meant higher.

The corporate additionally pulled off a giant acquisition not too long ago, buying ‘CAMSO’ to strengthen its off-highway tyre portfolio. That stated, the outcomes gained’t present up instantly. CEAT’s administration famous that full advantages from the mixing will take as much as two years:

“With the mixing of Camso straight away in FY ’26, we’ll hit the goal of 25% – 26% saliency of worldwide enterprise. So, integration is progressing properly, however we imagine the total advantages when it comes to value efficiencies and portfolio synergy will possible play out over the following 18 to 24 months.”

Trying forward, CEAT enters FY26 with a cautious outlook. It anticipates excessive single-digit income progress and secure margins, amidst main headwinds. Export demand stays comfortable, whereas current worth corrections in key segments like truck/bus radials and two-wheelers put stress on what it could possibly earn. And so, regardless of its ongoing investments in capability and expertise, the corporate’s near-term progress is anticipated to be gradual.

The Backside Line

For those who’re attempting to determine how one can spend money on any of those corporations, it’s not sufficient to simply take a look at three months’ outcomes. You could consider how prescient every of those are in how they see the auto business years from now.

MRF is betting that home substitute demand will stay king, and India’s market is large enough to maintain targeted progress. Apollo is betting that Indian tyre corporations might be international gamers, competing on expertise and high quality. JK Tyre is setting itself aside, betting on business automobile progress and export markets. CEAT is betting that expertise and manufacturing excellence will differentiate them in an more and more aggressive market.

In a rustic including thousands and thousands of automobiles yearly, transitioning (slowly) to electrical mobility, and increasing highway infrastructure, all 4 corporations are wrestling with the identical strategic puzzle: which elements of the tyre worth chain will probably be most worthwhile to personal over the following decade?

The rubber, fairly actually, remains to be hitting the highway on that reply.

Apple Distributors in India Cross 20% Native Worth Addition as iPhone Exports Contact ₹1.5 Trillion

Supply: Enterprise Normal

Apple’s key distributors in India — Tata Electronics, Foxconn, Pegatron, and Wistron — have surpassed the 20% home worth addition (DVA) mark, signaling a shift within the nation’s function in international electronics manufacturing. In line with authorities information, this threshold was achieved as the businesses ramped up native operations together with meeting, testing, and localisation of equipment. In FY25, iPhone exports from India reached ₹1.5 trillion, reflecting a 76% year-on-year enhance. This suggests roughly ₹30,000 crore of worth was generated inside India, assuming a 20% DVA. Different gamers like Samsung India and Padget Electronics have additionally crossed this 20% benchmark. The event marks a notable enchancment from only a few years in the past, when most distributors had DVA ranges in low single digits. Whereas China and Vietnam proceed to have larger DVA percentages in some classes, India’s progress underlines rising native capabilities.

JLR Cuts FY26 Margin Forecast to five–7%, Tata Motors Shares Drop Almost 5%

Supply: Reuters

Jaguar Land Rover has revised its EBIT margin steering for fiscal 2026 to five–7%, down from its earlier forecast of 10%. This up to date outlook additionally falls beneath the 8.5% margin the corporate reported within the earlier fiscal 12 months. The downgrade comes amid rising uncertainty within the international auto market, notably because of potential 25% tariffs on foreign-made automobiles within the U.S. market—the place JLR generates over 1 / 4 of its gross sales. In response to the tariff menace, the corporate has briefly paused shipments to the U.S., its second-largest market. Notably, JLR has no manufacturing presence within the U.S., not like rivals corresponding to BMW and Mercedes-Benz. The announcement has raised issues over the near-term profitability of Tata Motors, which depends considerably on JLR for its consolidated earnings.

Godrej Properties Acquires 14-Acre Bengaluru Land for ₹1,500 Crore Housing Venture

Supply: Enterprise Normal

Godrej Properties has acquired a 14-acre land parcel in Hoskote, East Bengaluru, for the event of a premium residential mission. The corporate expects to generate roughly ₹1,500 crore in income from this mission, which is able to supply round 1.5 million sq. toes of saleable space. This acquisition strengthens Godrej’s presence in East Bengaluru, a market the corporate considers strategically vital. The announcement follows an identical transfer earlier this month, the place Godrej acquired one other 14-acre parcel in Pune for ₹800 crore, focusing on a income potential of ₹4,200 crore throughout 3.7 million sq. toes. The corporate has not disclosed the price of the Bengaluru land acquisition.

This version of the e-newsletter was written by Kashish and Vignesh.

We’ve began a guide membership the place we meet every week in JP Nagar, Bangalore to learn and discuss books we discover fascinating.

For those who suppose you’d be severe about this and wish to be a part of us, we’d like to have you ever alongside! Take part right here.

Each week we hearken to the massive Indian earnings calls—Reliance, HDFC Financial institution, even the smaller logistics corporations—and replica the total transcripts. Then we bin the fluff and maintain solely the sentences that would transfer a share worth: a shock worth hike, a cut-back on manufacturing facility spending, a warning about weak monsoon gross sales, a touch from administration on RBI liquidity. We add a fast, one-line explainer and a timestamp so you possibly can hint the quote again to the decision. The entire thing lands in your inbox as one sharp web page of information you possibly can learn in three minutes—no 40-page decks, no jargon, simply the arduous stuff that issues to your trades and your macro view.

Go take a look at The Chatter right here.

“What the hell is occurring?”

We’ve been considering quite a bit about how one can make sense of a world that feels more and more unhinged – the place every part appears to be taking place directly and our common frameworks for understanding actuality really feel fully insufficient. This week, we dove deep into three huge shifts reshaping our world, utilizing what historian Adam Tooze calls “polycrisis” considering to attach the dots.

Frames for a Fractured Actuality – We’re struggling to grasp the current not from ignorance, however from poverty of frames – the psychological shortcuts we use to make sense of chaos. Historian Adam Tooze’s “polycrisis” idea captures our second of a number of interlocking crises higher than conventional analytical frameworks.

The Hidden Monetary System – A $113 trillion FX swap market operates off-balance-sheet, creating systemic dangers regulators barely perceive. Forex hedging by international insurers has basically modified how monetary crises unfold worldwide.

AI and Human Id – We’re dealing with humanity’s most profound identification disaster as AI matches our cognitive talents. Utilizing “disruption by default” as a body, we assume AI reshapes every part reasonably than dwelling in denial about job displacement that’s already taking place.

Subscribe to Aftermarket Report, a e-newsletter the place we do a fast every day wrap-up of what occurred within the markets—each in India and globally.

Thanks for studying. Do share this with your mates and make them as sensible as you might be ![]()

")