Introduction

Company conferences have lengthy been acknowledged as pivotal occasions in monetary markets, serving as catalysts that sign upcoming improvements and strategic shifts. Scheduled company occasions induce market reactions that may be systematically analyzed to disclose predictable return patterns. On this work, we deal with analyzing the return drift exhibited by expertise shares within the days surrounding their respective conferences, using easy quantitative strategies with every day value knowledge.

The hypothesized return drift is premised on the notion that investor sentiment and market dynamics are considerably altered by the data disseminated at these conferences. Traders, reacting to each anticipatory alerts and post-announcement changes, are inclined to drive costs in a measurable method within the home windows instantly previous, throughout, and after the occasions. By systematically analyzing shares of corporations resembling Apple, Google, and Microsoft, this examine goals to validate the existence of those drift patterns and make clear the underlying mechanisms, thereby enhancing mutual understanding of event-driven asset pricing dynamics.

Background

The affect of scheduled company occasions on inventory market conduct has been extensively documented within the finance literature. Early seminal work by Cutler et al. (1989) and subsequent analyses by Fama (1998) present a theoretical framework that helps the concept info flows throughout such occasions can quickly distort market costs. These research are complemented by extra up to date investigations (e.g., Brennan, Huh, and Subrahmanyam, 2018), which have utilized high-frequency knowledge methodologies to uncover delicate but statistically vital return changes round key company bulletins. Our evaluation builds on this foundational work by particularly correlating convention dates with empirical return outcomes within the expertise sector.

Parallel analysis has more and more targeted on the nuances of investor conduct within the context of event-driven buying and selling. Within the realm of expertise shares, conferences serve not solely as venues for product launches but in addition as alternatives for signaling future progress trajectories and strategic investments. Though the mixing of rising applied sciences, resembling synthetic intelligence, is a rising space of curiosity, our examine treats these components as secondary to the first narrative of innovation and market response. This distinction aligns with the insights offered by Baker and Wurgler (2007) and Hong and Stein (2007), who argue that whereas novel elements do affect market perceptions, the timing and construction of investor responses largely conform to classical occasion idea. Our examine contributes to this literature by offering a focused evaluation of the return drift phenomenon, supported by rigorous methodological execution and empirical validation.

Strategies

On this part, we’ll briefly define our thought course of, thought growth, and talk about the employed approaches, presenting preliminary and preliminary investigation outcomes that lay the groundwork for superior and additional work.

Information

Dates of conferences are from the corresponding Wikipedia pages, and correctness checked by a easy Google double-check (in case of Google convention, Google search is the first supply):

Monetary knowledge for corresponding shares AAPL, GOOGL (alternative of Class A shares is due to barely higher liquidity than Class C GOOG), and MSFT are from EODHD.com – the sponsor of our weblog. (All costs are dividend-adjusted and take inventory splits into consideration, so-called adjusted shut by knowledge supply.)EODHD affords seamless entry to +30 years of historic costs and basic knowledge for shares, ETFs, foreign exchange, and cryptocurrencies throughout 60+ exchanges, out there through API or no-code add-ons for Excel and Google Sheets. As a particular supply, our weblog readers can get pleasure from an unique 30% low cost on premium EODHD plans.

Our thought of knowledge pattern spans from September 12, 2011, to June 3, 2025.

Preliminary Evaluation

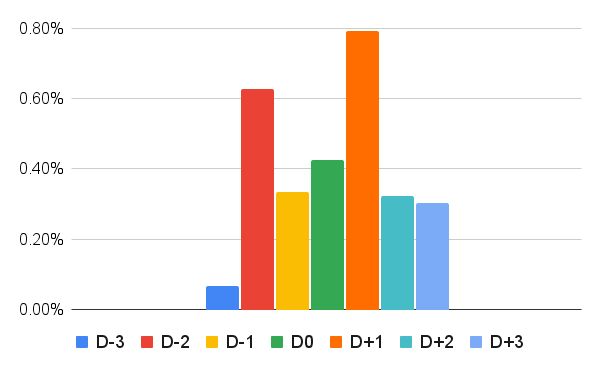

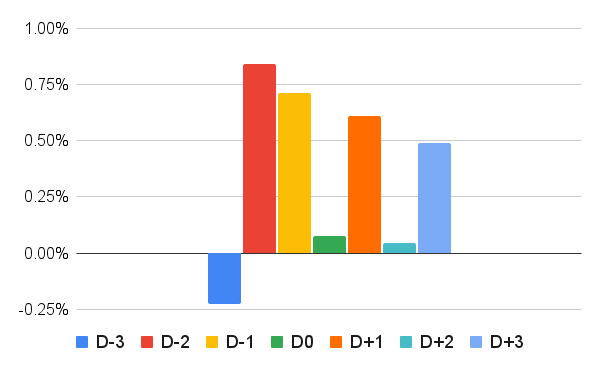

The primary kind of study concerned a easy investigation of the distribution of outcomes across the days previous (D-3 to D-1) and following (D+1 to D+3) the conferences. Right here, D0 represents the variety of days in the course of the convention, which can vary from one to 4, and averages the return over lately as if one holds inventory constantly.

The next are histograms presenting outcomes for every inventory in an lengthy place (purchase) and its respective convention:

We will see there’s a drift previous, throughout, and after the catalyst, on this case, the convention days. What it differs in is, after all, depth. The strongest is the anticipatory run, which the previous buying and selling adage of hypothesis knowledge characterised as: “Purchase the rumor, promote the information.” Nevertheless, post-conference drift can be not negligible, particularly within the case of Apple and Google.

Outcomes

As we usually do, after conducting preliminary investigations and easy analyses, we intention to develop an actionable buying and selling technique to create a helpful and sensible funding technique primarily based on the exploitable findings.

We evaluated a number of choices, starting from previous and following days, and located a simple but highly effective mixture to attain probably the most optimum outcomes.

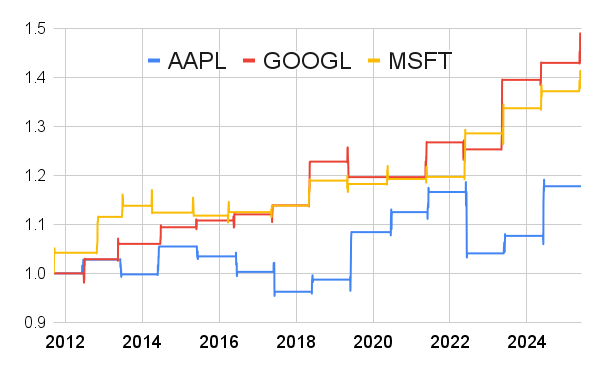

Convention Drift for Particular person Shares

We develop an idea of a straightforward buying and selling technique that holds lengthy positions (buys) in any of the three talked about shares throughout a time window from D-2 to D+2.

We will see that every of the shares reveals a reasonably optimistic efficiency and regular returns, aside from Apple, which has been barely lagging behind its friends. Developer conferences, within the case of Apple, are most likely not the one which takes probably the most consideration, and value motion is maybe centered additionally round different occasions (like September’s announcement of recent Apple merchandise).

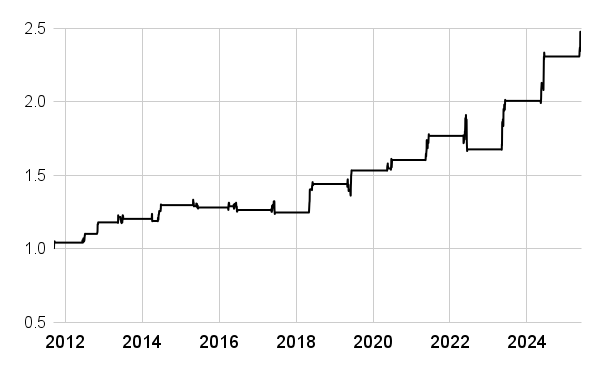

Remaining Technique Growth

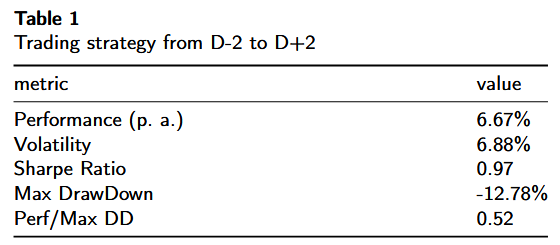

So, what does the efficiency of a “purchase and maintain” portfolio of those three shares throughout D-2 and D+2 of their convention days appear like?

As a normal of our reporting, we current probably the most important efficiency and threat metrics to judge the technique:

Technique reveals regular returns with occasional sharp drawdown. Benefit of technique is allocation to shares solely few days a yr whereas making an attempt solely to seize optimistic conduct primarily based on inner inventory fundamentals.

Market Impartial Technique (Alpha Era)

The concept right here is to make use of a market-neutral technique, supplementing the ultimate plan with a brief SPY leg, thereby successfully creating a variety portfolio that captures the surplus (alpha) return primarily based on the generated sign.

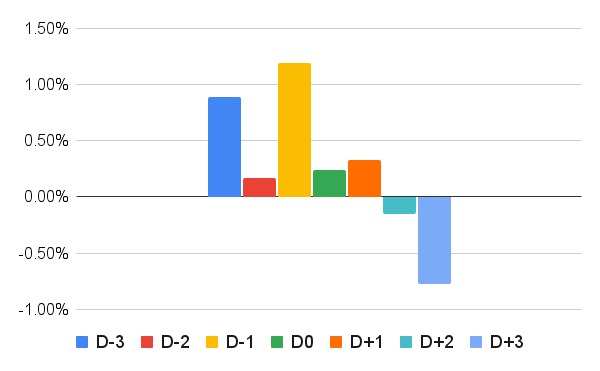

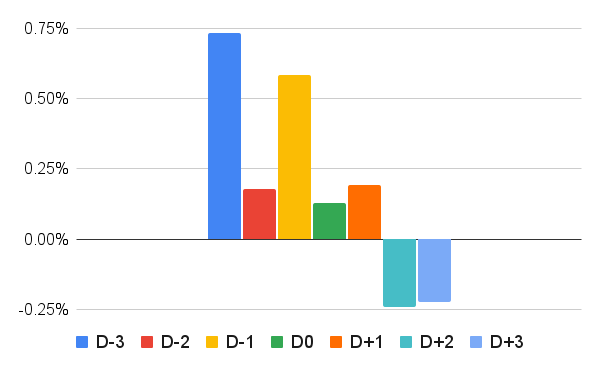

To confirm and validate the generated sign, we created a histogram of the corresponding inventory’s returns on days surrounding conferences and subtracted the return from the broad market, represented on this case by the SPY ETF.

It’s nonetheless evident that a good portion of returns comes from D-2 to D+1, and capturing these market-independent returns is essential.

MSFT and GOOGL are once more higher performing, whereas AAPL lags. As soon as once more, probably the most possible rationalization is that the developer conferences should not occasions when many of the AAPL value motion takes place.

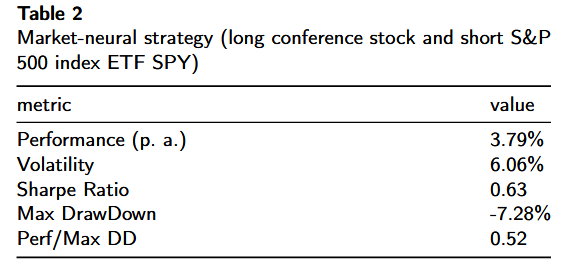

Market-Impartial Technique

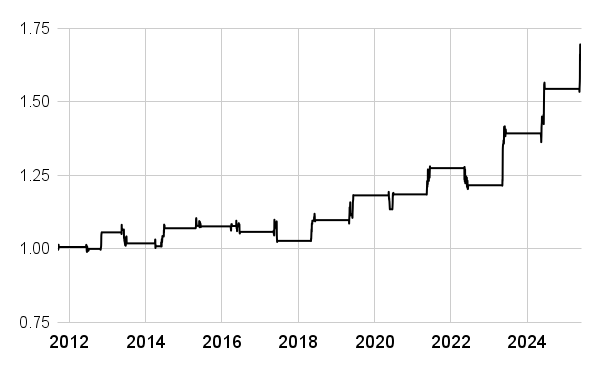

The rule right here is to be lengthy convention inventory and brief SPY, however solely on days D-2 to D+2 to make it comparable with our first simple long-only technique.

Whereas this technique affords a decrease return, it additionally reveals decrease drawdown and achieves independence from the efficiency of the general broad inventory market, thereby providing a helpful further alternative for portfolio managers searching for to seize alpha.

Conclusions

The empirical outcomes derived from the D-2 to D+2 buying and selling technique underscore a compelling market inefficiency that manifests round main expertise conferences. Particularly, our technique achieved an annualized efficiency of 6.67%, with a volatility of 6.88% and a Sharpe Ratio of 0.97, whereas recording a most drawdown of -12.78% and a performance-to-drawdown ratio of 0.52. These efficiency metrics not solely validate the robustness of a method that capitalizes on the return drift phenomenon but in addition affirm that the scheduling of those occasions considerably influences investor conduct, thereby predictably distorting asset pricing.

Our evaluation establishes that the return drift noticed within the D-2 to D+2 window represents a worthwhile anomaly throughout the broader context of event-driven buying and selling. By systematically correlating convention dates with tangible return outcomes, we offer empirical proof of a market inefficiency. This anomaly, as evidenced by the statistically vital and repeatable efficiency metrics obtained, presents a engrossing case examine on how systematic buying and selling methods that exploit transient pricing dislocations can obtain superior risk-adjusted returns, thereby contributing to each the tutorial literature and sensible buying and selling paradigms.

Creator: Cyril Dujava, Quant Analyst, Quantpedia

Are you on the lookout for extra methods to examine? Join our publication or go to our Weblog or Screener.

Do you wish to study extra about Quantpedia Premium service? Test how Quantpedia works, our mission and Premium pricing supply.

Do you wish to study extra about Quantpedia Professional service? Test its description, watch movies, assessment reporting capabilities and go to our pricing supply.

Are you on the lookout for historic knowledge or backtesting platforms? Test our record of Algo Buying and selling Reductions.

Would you want free entry to our providers? Then, open an account with Lightspeed and luxuriate in one yr of Quantpedia Premium for gratis.

Or comply with us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookConfer with a good friend

")