Authors: Nihad Aliyev, Matteo Aquilina, Khaladdin Rzayev, Xingyu Sonya Zhu

Title: Via Stormy Seas: How Fragile is Liquidity Throughout Asset Lessons?

Hyperlink: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5254046

Summary:

Liquidity has improved throughout world markets, however fragility considerations stay. We research the distribution of bid-ask spreads throughout equities, bonds, and overseas alternate (FX) within the US, Europe and Japan. Whereas common and normal deviation of spreads have decreased since Nineteen Nineties, skewness and kurtosis have elevated, particularly in bond and most fairness markets, however not FX. We determine structural breaks within the imply and skewness and map them to macroeconomic occasions, market construction adjustments, and regulatory reforms. Simulations present that elevated skewness raises buying and selling costs-up to $1 billion yearly in US equities-even when few trades require pressing execution.

As ever, we current a number of fascinating figures and tables:

Notable quotations from the tutorial analysis paper:

“[…] we transcend common measures of liquidity and study how higher-order moments of its distribution, particularly skewness and kurtosis, have developed over time. Our intention is to grasp how liquidity behaves not solely in regular occasions but in addition within the tails in periods of stress when it issues most. We give attention to three main asset lessons: shares, authorities bonds, and overseas alternate (FX). These markets play a essential function in capital allocation, financial coverage transmission, and danger administration for governments, companies, and traders. We research the distribution of bid-ask spreads (and different liquidity measures for robustness) throughout the important thing developed markets of america, Europe, and Japan.1 To this finish, we compile a high- frequency dataset of relative bid-ask spreads, which we combination into month-to-month and annual metrics to seize the distribution of liquidity over time, throughout asset lessons, and throughout areas.

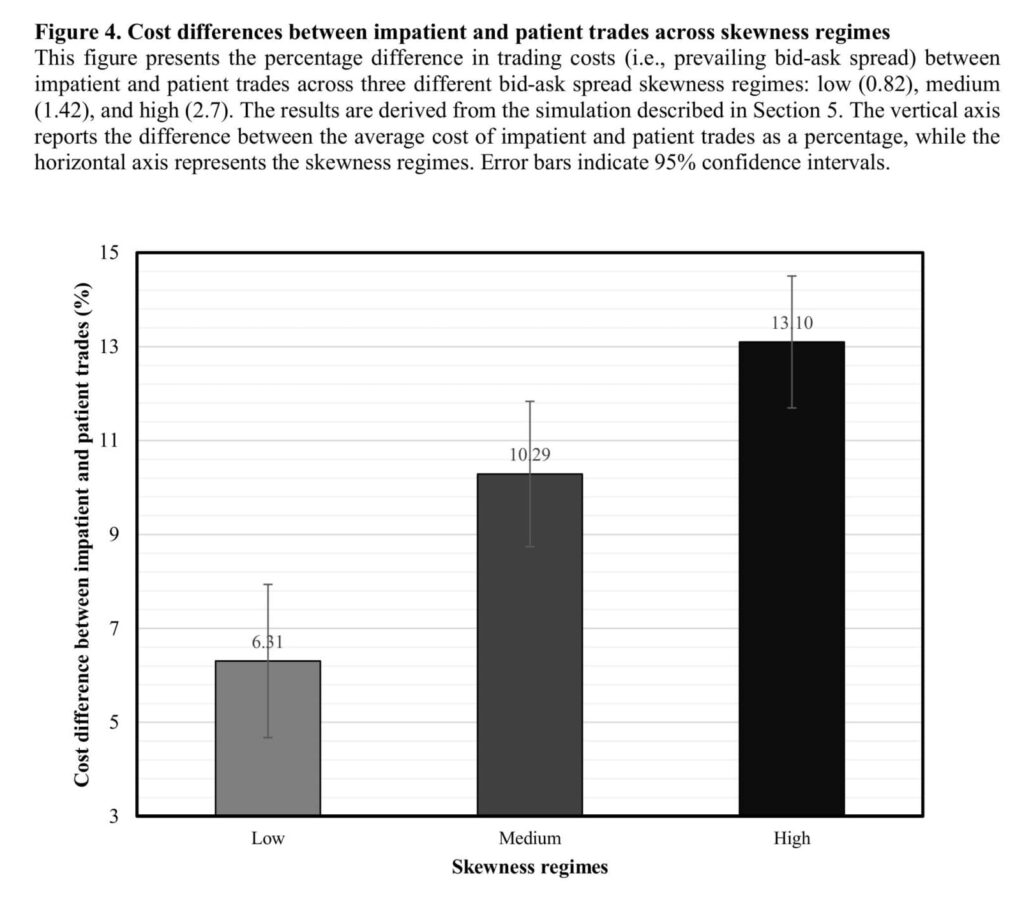

Simulation outcomes present that adjustments within the skewness of spreads can have significant results on buying and selling prices. We discover that shifting from the low-level of skewness of the late Nineteen Nineties to the high-level of US massive cap equities in 2023, the buying and selling value distinction between affected person and impatient trades turns into considerably bigger. Within the low-skewness setting, the premium paid for speedy execution is round 6%, however it greater than doubles to 13% within the excessive skewness setting. When the chance of being impatient is low, total buying and selling prices stay comparable throughout totally different skewness ranges as merchants can look forward to the unfold to revert. Nonetheless, because the chance of impatience will increase—a situation extra doubtless throughout market stress—buying and selling prices improve rapidly in high-skewness regime.

[…] First, to our information, we’re the primary to doc how the distribution of liquidity has developed throughout three main asset lessons (equities, authorities bonds, and FX) within the main world markets of the US, Europe, and Japan, drawing on a dataset of over 2 billion high-frequency observations. This broader perspective is vital as a result of it permits us to match patterns throughout markets that differ in construction, members, and regulation. For instance, FX markets—the place common spreads have decreased however skewness has not elevated—could supply helpful insights into mechanisms that protect the resilience of liquidity. Understanding these variations can assist determine which features of market design contribute to extra steady liquidity and what structural options one market may undertake from one other to enhance the resilience of liquidity.Second, we transcend describing tendencies and determine potential drivers of each imply and skewness of liquidity and hyperlink them to macroeconomic occasions, market construction, and regulation throughout totally different markets and areas. This enables us to disentangle the components related to enhancements in common liquidity from these contributing to its elevated fragility. Third, we quantify the buying and selling value implications of skewed liquidity utilizing simulations. We present that increased skewness in spreads, even when common circumstances are steady, can improve prices for merchants who have to execute rapidly. Collectively, our findings present new proof on what makes liquidity fragile throughout totally different markets and why that issues for market members.”

Are you in search of extra methods to examine? Join our e-newsletter or go to our Weblog or Screener.

Do you wish to be taught extra about Quantpedia Premium service? Test how Quantpedia works, our mission and Premium pricing supply.

Do you wish to be taught extra about Quantpedia Professional service? Test its description, watch movies, overview reporting capabilities and go to our pricing supply.

Are you in search of historic information or backtesting platforms? Test our record of Algo Buying and selling Reductions.

Would you want free entry to our providers? Then, open an account with Lightspeed and luxuriate in one 12 months of Quantpedia Premium for gratis.

Or observe us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookConsult with a good friend

")