By Mohak Pachisia

TL;DR

Most traders concentrate on choosing shares, however asset allocation, the way you distribute your investments, issues much more. Whereas poor allocation may cause concentrated dangers, a methodical method to allocation would result in a extra balanced portfolio, higher aligned with the portfolio goal.

This weblog explains why Threat Parity is a robust technique. Not like equal-weighting or mean-variance optimisation, Threat Parity allocates primarily based on every asset’s threat (volatility), aiming to steadiness the portfolio in order that no single asset dominates the chance contribution.

A sensible Python implementation exhibits tips on how to construct and examine an Equal-Weighted Portfolio vs. a Threat Parity Portfolio utilizing the Dow Jones 30 shares.

Key outcomes:

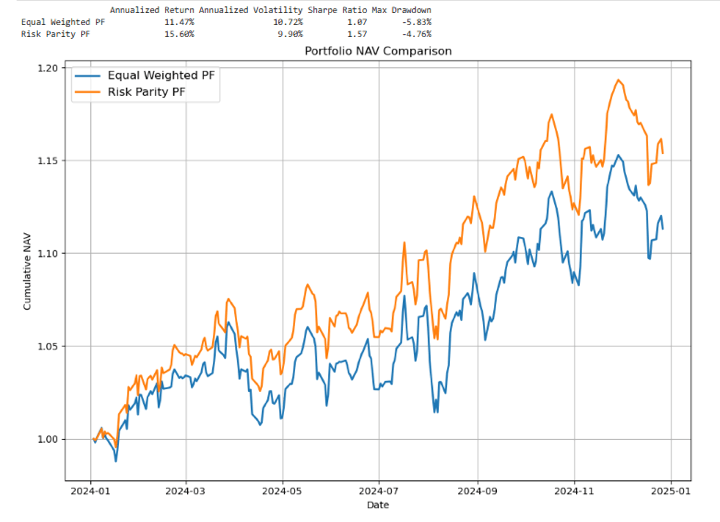

Threat Parity outperforms with increased annualized return (15.6% vs. 11.5%), decrease volatility (9.9% vs. 10.7%), higher Sharpe ratio (1.57 vs. 1.07), and smaller max drawdown (-4.8% vs. -5.8%).Whereas compelling, Threat Parity is determined by historic volatility, it wants frequent rebalancing, and should underperform in sure market situations.

To get probably the most out of this weblog, it’s useful to be aware of a number of foundational ideas.

Pre-requisites

First, a stable understanding of Python fundamentals is crucial. This contains working with primary programming constructs in addition to libraries regularly utilized in information evaluation. You may discover these ideas in-depth via Fundamentals of Python Programming.

For the reason that weblog builds on monetary information dealing with, you’ll additionally have to be snug with inventory market information evaluation. This entails studying tips on how to acquire market datasets, visualise them successfully, and carry out exploratory evaluation in Python. For this, try Inventory Market Knowledge: Acquiring Knowledge, Visualization & Evaluation in Python.

By masking these stipulations, you’ll be well-prepared to dive into the ideas mentioned on this weblog and apply them with confidence.

Desk of contents

Ever puzzled the place your portfolio’s threat is coming from?

Most traders focus closely on choosing the right shares or funds, however what if the best way you allocate your capital is extra necessary than the property themselves? Analysis constantly exhibits that asset allocation is the important thing driver of long-term portfolio efficiency. For instance, Vanguard has printed a number of papers reinforcing that asset allocation is the dominant think about portfolio efficiency.

On this put up, we take a more in-depth take a look at Threat Parity, a sensible and systematic method to portfolio building that goals to steadiness threat, not simply capital. As an alternative of letting one asset class dominate your portfolio’s threat, Threat Parity spreads publicity extra evenly, probably resulting in better stability throughout market cycles.

Quantitative Portfolio Administration is a 3-step course of.

Asset selectionAsset AllocationPortfolio rebalance and monitoring

In trendy portfolio idea, analysis has proven that “Asset Allocation” has performed a serious function in portfolio efficiency. We’ll perceive Asset Allocation in-depth after which transfer to understanding one of many potential methods to allocate property, the Hierarchical Threat Parity methodology.

What’s Asset Allocation?

Allow us to take an instance of a novice investor. This investor has a portfolio of 5 shares and has invested $30,000 in them.

How he/she purchased particular proportions of the shares might depend upon subjective evaluation or on the funds they’ve now to purchase shares. And this results in a random publicity of various shares. As given beneath, let’s assume that the novice investor is shopping for shares, and that is how the allocation seems to be:

Observe: Among the numbers beneath may very well be approximations, for demonstration functions.

Shares

Costs

Shares

Publicity

AAPL

243

8

1944

MSFT

218

20

4366

AMZN

190

19

3610

GOOGL

417

20

8340

NVDA

138

85

11742

Whole

30000

Consequently, the proportion of every inventory purchased would broadly range.

Observe: The variety of shares is just not an entire quantity. The calculations are approximations just for demonstration functions.

Shares

Costs

Shares

Publicity

% weights

AAPL

243

8

1946

6%

MSFT

218

20

4366

15%

AMZN

190

19

3610

12%

GOOGL

417

20

8336

28%

NVDA

138

85

11742

39%

Whole

30000

100%

We clearly see that NVDA has a considerably increased weightage of 39% whereas APPL has merely a weightage of 6%. There’s a nice disparity within the allocation of funds throughout the totally different shares.

Case 1: NVDA underperforms; it’s going to have a major influence in your portfolio. Which might result in massive drawdowns, and that is excessive idiosyncratic threat.

Case 2: APPL outperforms, because of a a lot decrease weightage of the inventory in your portfolio. You gained’t profit from it.

How Can We Clear up This Allocation Imbalance?

Quantitative Portfolio Managers don’t allocate funds primarily based on subjectivity. It’s trade observe to undertake logical, examined, and efficient methods to do it.

Uneven fund allocation can expose your portfolio to concentrated dangers. To handle this, a number of systematic asset allocation methods have been developed. Let’s discover probably the most notable ones:

1. Equal Weighting:

Strategy: Assigns equal capital to every asset.

Observe: The variety of shares is just not an entire quantity. The calculations are approximations just for demonstration functions.

Shares

Costs

Shares

Publicity

% weights

AAPL

243

24.7

6000

20%

MSFT

218

27.5

6000

20%

AMZN

190

31.6

6000

20%

GOOGL

417

14.4

6000

20%

NVDA

138

43.4

6000

20%

Whole

30000

100%

Professionals: Easy, intuitive, and reduces focus threat.Cons: Ignores variations in volatility or asset correlation. Might overexpose to riskier property.

Actual world instance: MSCI World Equal Weighted Index

2. Imply-Variance Optimisation (MVO)

Strategy: Based mostly on Trendy Portfolio Idea, it goals to maximise anticipated return for a given stage of threat. Although it seems to be easy, this method is adopted by a number of fund managers; its effectiveness comes with periodically rebalancing the portfolio exposures :

Anticipated returnsAsset volatilitiesCovariances between property

Observe: The variety of shares is just not an entire quantity. The calculations are approximations just for demonstration functions.

Shares

Anticipated Return (%)

Volatility (%)

Optimised Weight (%)

Publicity ($)

Shares

AAPL

9

22

12%

3600

14.8

MSFT

10

18

18%

5400

24.8

AMZN

11

25

25%

7500

39.5

GOOGL

8

20

15%

4500

10.8

NVDA

13

35

30%

9000

65.2

Whole

100%

30000

Monte Carlo simulation is usually used to check portfolio robustness throughout totally different market eventualities. To know this methodology higher, please learn Portfolio Optimisation Utilizing Monte Carlo Simulation.

The plot beneath exhibits an instance of how portfolios with totally different anticipated returns and volatilities are created utilizing the Monte Carlo Simulation methodology. Hundreds, if no more, mixtures of weights are thought-about on this course of. The portfolio weights with the very best Sharpe ratio (marked as +) are sometimes taken because the portfolio with probably the most optimum weightages.

Observe: That is just for demonstration functions, not for shares used for our instance.

Professionals: Theoretically optimum: When inputs are correct, MVO can assemble probably the most environment friendly portfolio on the risk-return frontier.Cons: Extremely delicate to enter assumptions, particularly anticipated returns, that are tough to forecast.

3. Threat-Based mostly Allocation: Threat Parity

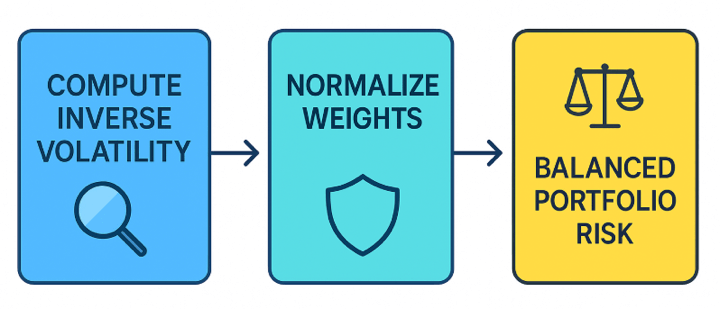

Strategy: As an alternative of allocating capital equally or primarily based on returns, Threat Parity allocates primarily based on threat contribution from every asset. The objective is for every asset to contribute equally to the full portfolio volatility. The method to attain this contains the next steps.

Estimate every asset’s volatilityCompute the inverse of volatility (i.e., decrease volatility → increased weight).Normalise the inverse of volatility to get last weights.

What’s volatility?

Volatility refers back to the diploma of variation within the value of a monetary instrument over time. It represents the pace and magnitude of value modifications, and is usually used as a measure of threat.

In easy phrases, increased volatility means better value fluctuations, which might indicate extra threat or extra alternative.

Components for Commonplace Deviation:

$$sigma = sqrt{frac{1}{N-1}sum_{i=1}^N (r_i – bar{r})^2}$$

[

begin{aligned}

text{where,}

&bullet sigma = text{Standard deviation}

&bullet r_i = text{Return at time } i

&bullet bar{r} = text{Average return}

&bullet N = text{Number of periods}

end{aligned}

]

Inverse of Volatility:

The inverse of volatility is just the reciprocal of volatility. It’s typically used as a measure of risk-adjusted publicity or to allocate weights inversely proportional to threat in portfolio building.

σ=Volatility

Then the Inverse of Volatility is: 1/σ

Normalise the inverse of volatility to get last weights :

To find out the ultimate portfolio weights, we take the inverse of every asset’s volatility after which normalise these values in order that their sum equals 1. This ensures property with decrease volatility obtain increased weights whereas sustaining a totally allotted portfolio.

[

w_i = frac{tfrac{1}{sigma_i}}{sum_{j=1}^N tfrac{1}{sigma_j}}

]

$$

textual content{The place,}

bullet w_i quad textual content{= weight of asset $i$ within the portfolio}

bullet sigma_i quad textual content{= volatility (normal deviation of returns) of asset $i$}

bullet N quad textual content{= complete variety of property within the portfolio}

bullet sum_{j=1}^N tfrac{1}{sigma_j} quad textual content{= sum of the inverse volatilities of all property}

$$

Instance of Threat Parity weighted method(making use of the above method):

The variety of shares is just not an entire quantity. The calculations are approximations just for demonstration functions.

Shares

Costs

Volatility (%)

1 / Volatility

Threat Parity Weight (%)

Publicity ($)

Shares

AAPL

243

24

0.0417

18.50%

5,550

22.8

MSFT

218

20

0.05

22.20%

6,660

30.6

AMZN

190

18

0.0556

24.60%

7,380

38.8

GOOGL

417

28

0.0357

15.80%

4,740

11.4

NVDA

138

30

0.0333

18.90%

5,670

41.1

Whole

100%

30,000

End result: No single asset dominates the portfolio threat.

Observe:

Volatility is an instance primarily based on an assumed % normal deviation.“Threat Parity Weight” is proportional to 1 / volatility, normalised to 100%.The publicity is calculated as: Threat Parity Weight × Whole Capital.Shares = Publicity ÷ Worth.

Professionals:

Doesn’t depend on anticipated returns.Easy, sturdy, and makes use of observable inputs.Reduces portfolio drawdowns throughout risky durations.

Cons:

Might obese low-volatility property (e.g., bonds), underweight development property.Ignores correlations between property (in contrast to HRP).

Different Allocation Strategies to Know:

Methodology

Core Concept

Notes

Hierarchical Threat Parity (HRP)

Makes use of clustering to detect asset relationships and allocates threat accordingly.

Solves issues of MVO like overfitting and instability.

Minimal Variance Portfolio

Allocates to minimise complete portfolio volatility.

Could be very conservative — typically heavy on low-volatility property.

Most Diversification

Maximises the diversification ratio (return per unit of threat).

Intuitive for decreasing dependency on anybody asset.

Black-Litterman Mannequin

Enhances MVO by combining market equilibrium with investor views.

Helps stabilise MVO with extra lifelike inputs.

Issue-Based mostly Allocation

Allocates to threat components (e.g., worth, momentum, low volatility).

Widespread in sensible beta and institutional portfolios.

Threat Parity Allocations Course of in Python

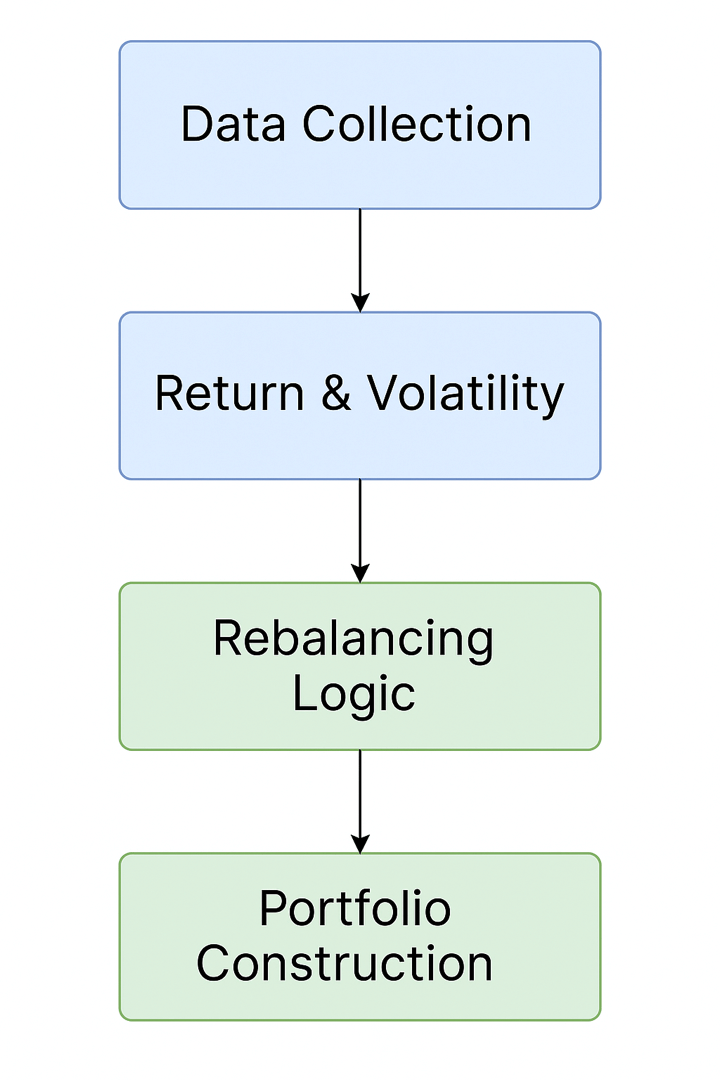

Step 1: Let’s begin by importing the related libraries

Step 2: We fetch the information for 30 shares utilizing their Yahoo Finance ticker symbols.

These 30 shares are the present 30 constituents of the Dow Jones Industrial Common Index.We fetch the information from one month earlier than 2024 begins. And goal a window of your complete yr 2024. That is completed as a result of we use a 20-day rolling interval to compute volatilities and rebalance the portfolios. 20 buying and selling days roughly interprets to at least one month.Solely the “Shut” costs are extracted, and the information body is flattened for additional evaluation.

Step 3: We create a operate to compute the returns of portfolios which can be both equally weighted or weighted utilizing the Threat Parity method.

Objective: To compute a portfolio’s cumulative NAV (Web Asset Worth) utilizing equal-weighted or risk-parity rebalancing at fastened intervals.

price_df: DataFrame containing historic value information of a number of property, listed by date.rebalance_period (default = 20):Variety of buying and selling days between every portfolio rebalancing.methodology (default=”equal”):Portfolio weighting methodology – both ‘equal’ for equal weights or ‘risk_parity’ for inverse volatility weights.

Step-by-Step Logic

Day by day Returns Calculation: The operate begins by computing each day returns utilizing pct_change() on the value information and dropping the primary NaN row.

Rolling Volatility Estimation: A rolling normal deviation is computed over the rebalance window to estimate asset volatility. To keep away from look-ahead bias, that is shifted by sooner or later utilizing .shift(1).

Begin Alignment: The earliest date all rolling volatility is on the market is recognized. The returns and volatility DataFrames are trimmed accordingly.

NAV Initialisation: A brand new Collection is created to retailer the portfolio NAV, initialised at 1.0 on the primary legitimate date.

Rebalance Loop: The operate loops via the information in home windows of rebalance_period days:

Volatility and Weights on Rebalance Day: On the primary day of every window:

Cumulative Returns & NAV Computation: The window’s cumulative returns are calculated and mixed with weights to compute the NAV path.

NAV Normalisation: The NAV is normalised to match the final worth of the earlier window, guaranteeing easy continuity.

Closing Output: Returns a time collection of the portfolio’s NAV, excluding any lacking values.

Step 4: Portfolio Building

We now proceed to assemble two portfolios utilizing the historic value information. This entails calling the portfolio building operate outlined earlier. Particularly, we generate:

An Equal-Weighted Portfolio, the place every asset is assigned the identical weight at each rebalancing interval.A Threat Parity Portfolio, the place asset weights are decided primarily based on inverse volatility, aiming to equalise threat contribution throughout all holdings.

Each portfolios are rebalanced periodically primarily based on the required frequency.

Step 5: Portfolio Efficiency Analysis

On this step, we consider the efficiency of the 2 constructed portfolios: Equal-Weighted and Threat Parity, by computing key efficiency metrics:

Day by day Returns: Calculated from the cumulative NAV collection to watch day-to-day efficiency fluctuations.Annualised Return: Derived utilizing the compound return over your complete funding interval, scaled to replicate yearly efficiency.Annualised Volatility: Estimated from the usual deviation of each day returns and scaled by the sq. root of 252 buying and selling days to annualise.Sharpe Ratio: A measure of risk-adjusted return, computed because the ratio of annualised return to annualised volatility, assuming a risk-free fee of 0.Most Drawdown: The utmost noticed peak-to-trough decline in portfolio worth, indicating the worst-case historic loss.

These metrics supply a complete view of how every portfolio performs when it comes to each return and threat. We additionally visualise the cumulative NAVs of each portfolios to watch their efficiency developments over time.

Regularly Requested Questions

What precisely is Threat Parity?

Threat Parity is a portfolio allocation technique that assigns weights such that every asset contributes equally to the full portfolio volatility, relatively than merely allocating equal capital to every asset. The objective is to forestall any single asset or asset class from dominating the portfolio’s total threat publicity.

How does it differ from Equal Weighting or Imply-Variance Optimisation?

Equal Weighting: This methodology allocates the identical quantity of capital to every asset. It’s easy and intuitive, however doesn’t take into account the chance (volatility) of every asset, probably resulting in concentrated threat.Imply-Variance Optimisation (MVO): Based mostly on Trendy Portfolio Idea, MVO seeks to maximise anticipated return for a given stage of threat by contemplating anticipated returns and covariances. Nonetheless, it’s extremely delicate to the accuracy of enter forecasts.Threat Parity: As an alternative of specializing in returns or allocating equal capital, Threat Parity adjusts weights primarily based on the volatility of every asset, allocating extra capital to lower-volatility property to equalise their threat contributions.

Why is asset allocation so necessary?

Analysis has proven that asset allocation is the first driver of long-term portfolio returns, much more important than choosing particular person securities. A well-thought-out allocation helps handle threat and enhances the chance of assembly funding targets.

How is volatility calculated in Threat Parity?

Volatility is usually measured as the usual deviation of previous returns over a rolling window (for instance, a 20-day rolling normal deviation). In Threat Parity, property with decrease volatility are assigned increased weights to steadiness their contribution to complete portfolio threat.

Is there Python code to implement this?

Sure. The weblog supplies full Python code examples utilizing libraries similar to pandas for information dealing with, yfinance for fetching historic costs, and customized capabilities to rebalance portfolios both by equal weights or by inverse volatility (Threat Parity).

Does Threat Parity all the time outperform different methods?

No. Whereas Threat Parity typically results in extra secure efficiency and higher risk-adjusted returns, particularly in diversified or risky markets, it could underperform easier methods like Equal-Weighted portfolios throughout robust bull markets that favour high-risk property.

What are the restrictions of Threat Parity?

It depends on the historic volatility to set goal weights, which can not precisely replicate the long run behaviour of property, particularly throughout abrupt modifications or crises.It usually requires frequent rebalancing, which might enhance transaction prices and potential slippage.It might under-allocate to high-growth property in trending markets, limiting upside in robust rallies.

Are there extra superior strategies past normal Threat Parity?

Sure. For instance, Hierarchical Threat Parity (HRP) makes use of clustering to know asset relationships and goals to allocate threat extra effectively by addressing a few of the weaknesses of conventional mean-variance approaches, similar to instability because of enter sensitivity.

Conclusion

The comparative evaluation highlights the clear benefits of utilizing a Threat Parity method over a conventional Equal-Weighted portfolio. Whereas each portfolios ship optimistic returns, Threat Parity stands out with:

Increased Annualised Return (15.60% vs. 11.47%)Decrease Volatility (9.90% vs. 10.72%)Superior Threat-Adjusted Efficiency, as seen within the Sharpe Ratio (1.57 vs. 1.07)Smaller Max Drawdown (-4.76% vs. -5.83%)

These outcomes show that by aligning portfolio weights with asset threat (relatively than capital), the Threat Parity portfolio might improve return potential together with higher draw back safety and smoother efficiency over time.

The NAV chart additional reinforces this conclusion, exhibiting a extra constant and resilient development trajectory for the Threat Parity technique.

In abstract, for traders prioritising stability over development, Threat Parity gives a compelling different to standard allocation strategies.

A Observe on Limitations

Though the Threat Parity portfolio delivered stronger returns in the course of the interval taken in our instance, its efficiency benefit is just not assured in each market section. Like several technique, Threat Parity comes with limitations. It depends closely on historic volatility estimates, which can not all the time precisely replicate future market situations, particularly throughout sudden regime shifts or excessive occasions.

It tends to shine in portfolios that blend excessive‑ and low‑volatility property, like shares and bonds, the place equal capital allocation would in any other case focus threat.Nonetheless, if low‑volatility property underperform or if all property have comparable threat profiles,

Moreover, the technique typically requires frequent rebalancing, which might enhance transaction prices and introduce slippage. In robust directional markets, notably these favouring higher-risk property, easier methods like Equal-Weighted might outperform because of their better publicity to momentum.

Therefore, whereas Threat Parity supplies a scientific strategy to steadiness portfolio threat, it needs to be used with an understanding of its assumptions and sensible limitations.

Subsequent Steps:

After studying this weblog, chances are you’ll need to improve your understanding of portfolio design and discover methods that present extra construction to risk-return trade-offs.

place to start is with Portfolio Variance/Covariance Evaluation, which explains how asset correlations influence portfolio volatility. This can give you the inspiration to know why diversification works and the place it doesn’t.

From there, Portfolio Optimisation Utilizing Monte Carlo Simulation introduces a extra dynamic method. By operating hundreds of simulated outcomes, you may take a look at how totally different allocations behave below uncertainty and determine mixtures that steadiness threat and reward.

To spherical it off, Portfolio Optimisation Strategies walks via a variety of optimisation frameworks, masking classical mean-variance fashions in addition to different strategies, so you may examine their strengths and apply them in several market situations.

Working via these subsequent steps will equip you with sensible methods to analyse, simulate, and optimise portfolios, a talent set that’s vital for anybody seeking to handle capital with confidence.

You may discover all of those intimately within the Portfolio Administration & Place Sizing Studying Monitor, which incorporates the Quantitative Portfolio Administration course for a complete understanding of portfolio building and optimisation.

For these seeking to develop past portfolio idea into the broader realm of systematic buying and selling, test the Govt Programme in Algorithmic Buying and selling – EPAT. Its complete curriculum, led by prime school like Dr. Ernest P. Chan, gives a number one Python algorithmic buying and selling course for profession development. EPAT covers core buying and selling methods that may be tailored and prolonged to Excessive-Frequency Buying and selling. Get personalised help for specialising in buying and selling methods with stay challenge mentorship.

Disclaimer: This weblog put up is for informational and academic functions solely. It doesn’t represent monetary recommendation or a advice to commerce any particular property or make use of any particular technique. All buying and selling and funding actions contain important threat. All the time conduct your individual thorough analysis, consider your private threat tolerance, and take into account in search of recommendation from a certified monetary skilled earlier than making any funding choices.

")