Some might imagine that put-call parity in choices is only a theoretical idea with no sensible purposes, as arbitrage alternatives are unavailable to retail merchants.

We’ll present you the way it has sensible software in setting up risk-free trades.

And we aren’t speaking about arbitrage.

We had proven beforehand with the risk-free collar that risk-free trades are certainly attainable.

Right now, we present a distinct variation that is likely to be aptly named the risk-free butterfly collar.

Contents

In a earlier video, we mentioned how one can have interaction in choices buying and selling with out incurring a lack of capital in a portfolio.

It is because we will obtain risk-free curiosity from U.S. Treasury payments.

It’s these risk-free curiosity returns that allow risk-free buying and selling to be attainable.

If the curiosity acquired is greater than the outlined max threat of the commerce, then you’ve got a risk-free commerce.

The chance-free rate of interest is already factored into the costs of choices contracts.

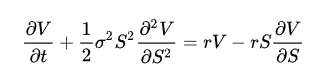

Simply have a look at the Black-Scholes choices pricing mannequin:

Supply: Wikipedia

It has the risk-free rate of interest “r” as one in every of its inputs.

As a sensible software, we are going to assemble a risk-free commerce that harnesses the free cash that’s embedded in sure inventory and choices by-product combos.

However first, we have to know what put-call parity is.

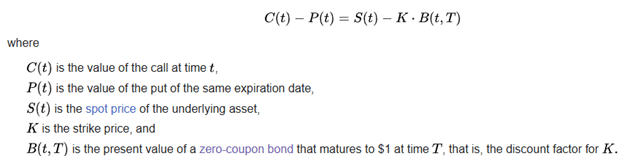

Put-call parity implies that the value of the decision possibility and the value of the put possibility (for a similar strike and expiration) are intimately linked.

Because the underlying asset value goes up, the decision possibility will increase in worth.

The put possibility (of the identical strike, expiration, and underlying) should synchronously lower in worth.

And vice versa.

It’s attainable to derive the value of the put possibility by figuring out the value of the decision possibility.

And vice versa.

As a result of the 2 costs should obey this system:

The final time period is the current worth of a zero-coupon bond. U.S. Treasury payments are one kind of zero-coupon bond, which earns a risk-free charge of return.

Once more, we see “free cash” coming into the equation.

As a result of if the value of the decision and the value of the put possibility don’t obey this system, there could be an arbitrage alternative.

In follow, arbitrage alternatives are scarce as a result of the market is extremely environment friendly, and algorithmic buying and selling helps preserve costs in line.

Nonetheless, we aren’t right here to have interaction in arbitrage.

Put-call parity permits us to assemble artificial positions.

For instance,

Lengthy name = lengthy inventory + lengthy put

Which means that having an extended name possibility is equal to proudly owning 100 shares of the underlying asset and holding an extended put possibility with the identical strike and expiration.

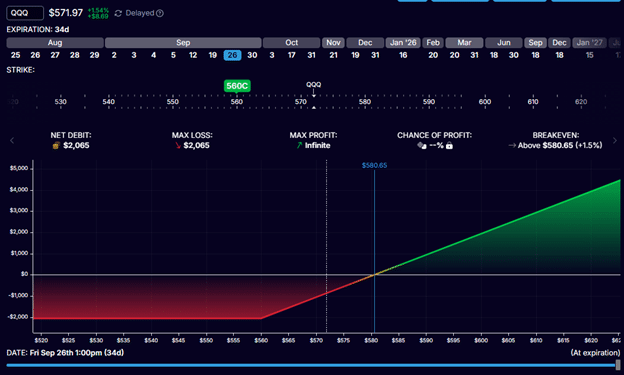

Suppose Investor Adam buys a 560-strike name possibility on QQQ expiring in 34 days on September 26, 2025.

Investor Adam paid $2065 to purchase this name possibility, and that may be the utmost attainable loss.

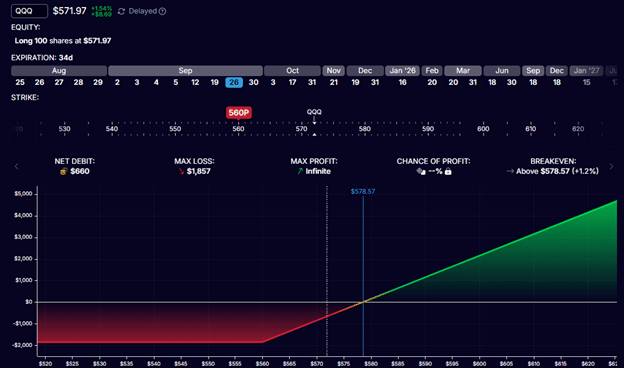

Investor Betty initiates an equal place by shopping for 100 shares of QQQ and shopping for a put possibility of the identical strike and expiration:

Price of 100 shares of QQQ: -$57,197

Price of 560-put possibility: -$660

Internet debit: -$57,857

Whereas Investor Adam paid $2065, Investor Betty paid $57,857 for another place that has an analogous payoff and threat profile.

We are saying related, however not 100% similar.

Investor Betty has a barely decrease most loss than Investor Adam:

Investor Betty’s max loss would happen when QQQ goes to zero.

In that case, Investor Betty can train the $ 560 put choice to obtain $560 per share.

Investor Betty max loss = $56,000 – $57,857 = -$1857

Recall that Investor Adam’s max loss is -$2065.

Why does Investor Betty have a decrease max threat than Investor Adam by about $208?

That is the “free cash” that the market is giving to Investor Betty as a result of she is fronting $57,857 of debit to be on this commerce.

Investor Betty has tied up $57,857 of money that might have been used elsewhere.

That is the “alternative value” of holding this commerce for 34 days.

This is named the “value of carry,” which is the price of holding an asset till a future date.

The market compensates Investor Betty for this additional “value”.

Who says the market isn’t truthful?

It’s as if Investor Betty had lent the market $57,857 and the market gave again a little bit of curiosity in return.

As a common precept, if in case you have a debit possibility place, the market will “provide you with again” some “curiosity”.

In case you have a credit score place, you pay up a little bit of “curiosity”.

Nonetheless, in a typical choices place, this curiosity is simply too small to even discover.

It turns into noticeable solely after we exchange an extended possibility with its inventory and equal put, which considerably will increase the debit.

How a lot is that this curiosity?

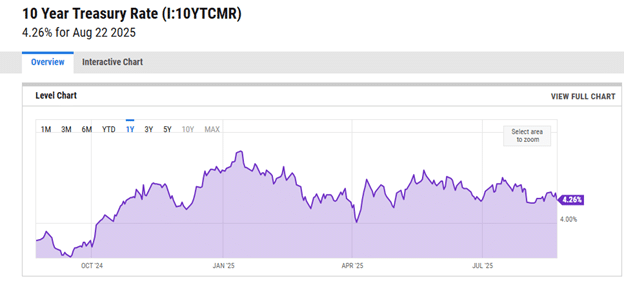

It’s in regards to the Federal Fund Charge or the risk-free charge of return.

Usually, the risk-free charge (as measured by treasury payments) carefully tracks the fed funds charge.

On this instance, a $208 return on $57,857 of capital over one month is roughly a 4% annualized return, near the present risk-free charge of return as measured by the 10-12 months Treasury charge.

Supply: ycharts.com

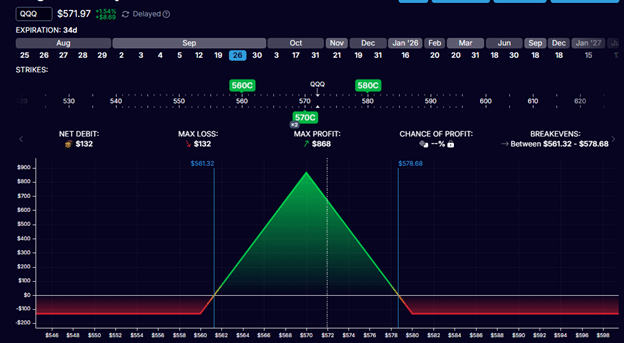

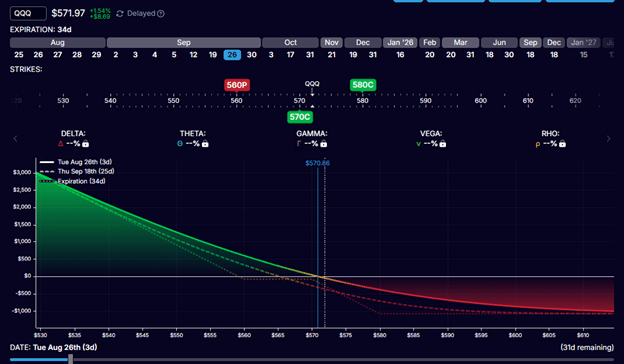

Taking the instance additional, suppose Investor Adam constructs an ordinary at-the-money butterfly with name choices:

Purchase one September 26 QQQ 580 name @ $7.78Sell two September 26 QQQ 570 name @ $13.56 eachBuy one September 26 QQQ 560 name @ $20.65

Internet debit: $132

Max threat: $132

Free Coated Name Course

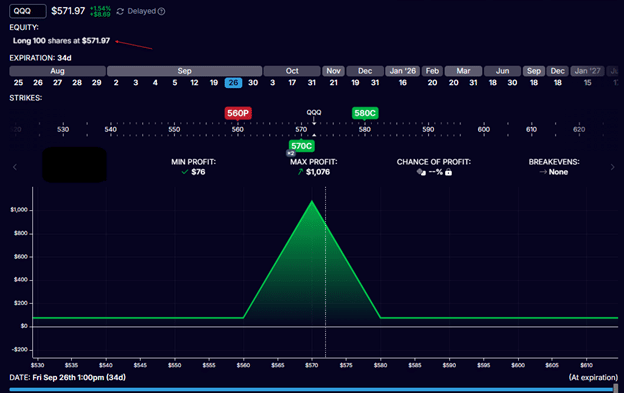

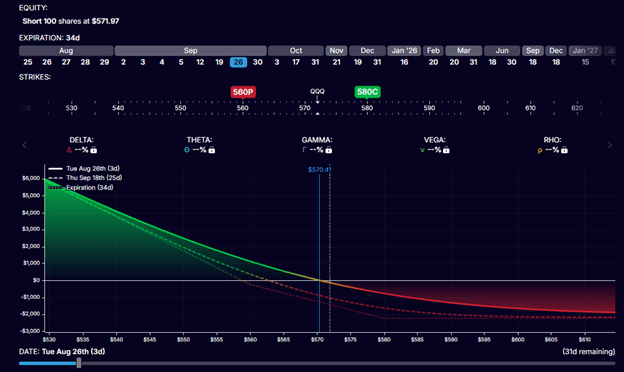

Investor Betty builds the identical commerce, however replaces the 560-call possibility with 100 shares of QQQ plus an $560-strike put possibility.

Purchase 100 shares of QQQ @ $571.97 per share

Purchase one September 26 QQQ 580 name @ $7.78Sell two September 26 QQQ 570 name @ $13.56 eachBuy one September 26 QQQ 560 put @ $6.60

Internet debit: -$55,924

Max threat: $0

Worst case: Revenue of $76

Finest case: Revenue of $1076

Within the worst-case situation, when QQQ goes to zero, all the decision choices and shares turn out to be nugatory.

The $560-strike put possibility would end in a lack of $56,000, which is $76 greater than the investor had initially invested within the commerce ($55,924).

Due to this fact, the commerce can’t lose cash – so long as it’s held to expiration.

The commerce can expertise a drawdown in some unspecified time in the future throughout the commerce.

And if the investor had exited the place at the moment, an actual loss would have been realized.

Within the worst-case situation, a $76 return on $55,924 of capital over 34 days is a 1.5% annualized return.

As a result of 76 / 55924 * 365 / 34 = 1.5% annualized

Sure, that is lower than the risk-free charge of return of 4%, which the investor may acquire just by shopping for some BIL.

Nonetheless, if the investor is ready to time and place the butterfly in such a manner that the value finally ends up contained in the expiration graph tent, the investor could possibly obtain a lot increased returns – maybe not the utmost acquire of $1076, however maybe $400 out of it.

In that case:

400 / 55924 * 365 / 34 = 7.6% annualized

The general annual return of the investor will fluctuate relying on the ability in studying the place the asset value will go, in addition to commerce administration abilities (when to exit).

If accomplished properly, the investor could make greater than the risk-free charge.

If accomplished poorly, the investor could be higher off investing in treasury payments.

On common, the risk-fee charge is more likely to be achieved.

However with nothing to lose, the investor can safely purpose for a better return.

Psychologically, the investor can be capable of maintain these trades longer to reap the bigger earnings that come into the butterfly solely when it will get nearer to expiration.

Why is Investor Betty capable of get a risk-free commerce, and Investor Adam isn’t?

As a result of Investor Betty is prepared to place up $55,924 of capital, Investor Adam solely put up $132.

If Investor Adam is prepared to place the remaining $55,792 into the BIL treasury ETF (returning about 4% yearly), then Investor Adam would have reaped $208 from the risk-free rate of interest:

$55792 x 0.04 x 34 / 365 = $208

This is able to have greater than coated the max lack of the butterfly plus a further $76 – practically precisely as Investor Betty.

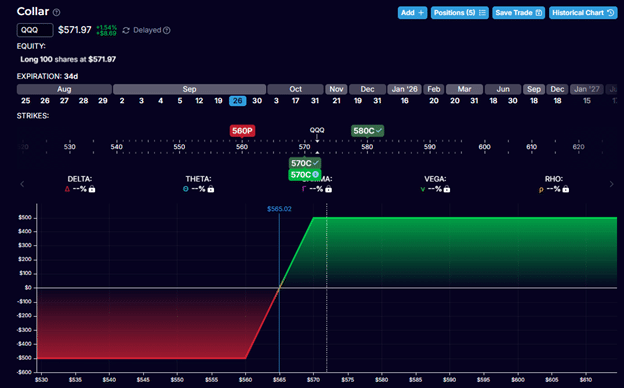

For those who group the legs of the above commerce like this:

Bear name unfold:

Purchase one September 26 QQQ 580 name @ $7.78Sell one September 26 QQQ 570 name @ $13.56

Choices Collar:

Promote one September 26 QQQ 570 name @ $13.56

Purchase 100 shares of QQQ @ $571.97Buy one September 26 QQQ 560 put @ $6.60

It’s actually simply an choices collar with a bear name unfold added.

That is what the choice collar appears to be like like:

By itself, it isn’t risk-free. Nonetheless, promoting the bear name unfold generates sufficient credit score to make it risk-free.

Within the above instance, we now have two brief calls at $570.

Having brief calls obligates the vendor to promote 100 shares of QQQ at any time when the opposite get together requests it.

The opposite get together is more likely to ask for it near the Ex-Dividend date when QQQ pays out a dividend to individuals who personal the shares earlier than the ex-dividend date.

Within the occasion that one brief name is exercised, the 100 shares of QQQ will likely be known as away, leaving a place with directional threat.

If each brief calls are exercised, the investor will likely be brief 100 shares of QQQ:

Leaving the place with directional threat (till the investor notices and closes out the complete place).

You possibly can commerce risk-free if in case you have sufficient capital to generate sufficient risk-free curiosity to offset any potential loss in a defined-risk commerce.

This additionally implies that these risk-free trades will NOT work in a zero-interest-rate surroundings (which we now have had previously).

The ultimate caveat is that there’s a low-probability threat of the brief choices being assigned early.

We hope you loved this text on risk-free trades utilizing put-call parity.

In case you have any questions, ship an electronic mail or go away a remark beneath.

Get Your Free Put Promoting Calculator

Commerce protected!

Disclaimer: The data above is for instructional functions solely and shouldn’t be handled as funding recommendation. The technique offered wouldn’t be appropriate for traders who are usually not acquainted with alternate traded choices. Any readers on this technique ought to do their very own analysis and search recommendation from a licensed monetary adviser.

")